If you're seeing this message, it means we're having trouble loading external resources on our website.

If you're behind a web filter, please make sure that the domains *.kastatic.org and *.kasandbox.org are unblocked.

To log in and use all the features of Khan Academy, please enable JavaScript in your browser.

Microeconomics

Course: microeconomics > unit 2, law of demand.

- Market demand as the sum of individual demand

- Substitution and income effects and the law of demand

- Price of related products and demand

- Change in expected future prices and demand

- Changes in income, population, or preferences

- Normal and inferior goods

- Inferior goods clarification

- What factors change demand?

- Lesson summary: Demand and the determinants of demand

- Demand and the law of demand

- The law of demand states that a higher price leads to a lower quantity demanded and that a lower price leads to a higher quantity demanded.

- Demand curves and demand schedules are tools used to summarize the relationship between quantity demanded and price.

Demand for goods and services

Demand schedule and demand curve.

- A demand schedule is a table that shows the quantity demanded at each price.

- A demand curve is a graph that shows the quantity demanded at each price. Sometimes the demand curve is also called a demand schedule because it is a graphical representation of the demand scheduls.

Attribution:

The difference between demand and quantity demanded, want to join the conversation.

- Upvote Button navigates to signup page

- Downvote Button navigates to signup page

- Flag Button navigates to signup page

- Learn Economics

- Teach High School

- Teach University

- We're Hiring

Courses See all

- Principles of Economics: Microeconomics

- Principles of Economics: Macroeconomics

- Mastering Econometrics

- Money Skills

- Development Economics

Series See all

- Everyday Economics

- Nobel Conversations

- Economists in the Wild

- Women in Economics

Interactive Practice See all

- Supply and Demand

Timely News Articles for Econ Class

Free high school teacher trainings, high school teaching resources see all.

- High School Economics

- AP Microeconomics

- AP Macroeconomics

- Personal Finance

- Lesson Plans

- Interactive Practice

- Assessments

University Teaching Resources See all

- Principles of Microeconomics

- Principles of Macroeconomics

- Assignments

Teacher Resources

Law of demand lesson plan.

See Lesson Plan

Request Answer Key

This 45-minute interactive lesson (in Google-Docs format) introduces the Law of Demand by engaging students with the media they use everyday, like our short instructional video on the demand curve.

But that's not the only way this lesson connects the demand curve to your students' lives: with current events, graphing exercises, and interactive games, this lesson keeps your students on their toes from the moment the bell rings to the time they turn in their exit ticket.

And of course, this step-by-step lesson has everything you need to use it immediately, including activity sheets, Google slides, and answer key. We also add ways for you to tailor the lesson to your class by providing additional resources like assessment questions, teacher tips, and engaging extension activities. And it's part of a 5-day unit on supply, demand, and equilibrium that is also chock full of engaging activities! Access it here .

Key economic concepts: quantity demanded, price, demand schedule, demand curve, law of demand, substitutes

Want the full unit on supply, demand, and equilibrium? Check it out here !

Request Answer Key

High School

Resource Details

Academic level, applicable courses.

- CEE Voluntary National Content Standards in Economics (Standard 8: Benchmark 12:1)

Other Related Content

Assignment: Amy Finkelstein on Selection and Screening of Mammograms

Econ in the News: Weekly Email of Real-World Econ Examples in the News!

- News Articles

Supply, Demand, and Equilibrium Unit Plan

Globalization, Robots, and You Unit Plan

More information about text formats

- No HTML tags allowed.

- Lines and paragraphs break automatically.

- Allowed HTML tags: <em> <strong> <cite> <blockquote> <code> <ul> <ol> <li> <dl> <dt> <dd> <br> <p>

Thanks for this well-conceived, timely and relevant lesson plan. I will follow-up with more direct feedback when I use it in my 12th grade general econ courses.

Thanks for the resources (╬▔皿▔)╯:D

Thanks for the great lesson.

Looks Great Thanks

Looking for more resources?

Sign up and receive updates on new videos, test banks, and classroom activities!

Send me more resources!

- Search Search Please fill out this field.

Consumer Demand

Explaining supply, finding equilibrium, the bottom line.

- Macroeconomics

Introduction to Supply and Demand

:max_bytes(150000):strip_icc():format(webp)/image0-MichaelBoyle-d90f2cc61d274246a2be03cdd144f699.jpeg "demand economics assignment")

The law of supply and demand is a fundamental concept of economics and a theory popularized by Adam Smith in 1776. The principles of supply and demand are effective in predicting market behavior. Whether an individual is a manufacturer or a consumer, the supply and demand equilibrium is relevant in daily market transactions.

Key Takeaways

- The law of supply and demand was popularized by Adam Smith in 1776.

- Consumer demand for a good commonly decreases as its price rises.

- As prices of a good increase, producers manufacture more to realize more profits.

Consumer demand for a good commonly decreases as its price rises. The figure below depicts the relationship between the price of a good and its demand from the consumer's standpoint. The demand curve is portrayed from the view of the consumer, whereas supply graphs are drawn from the producer's perspective.

If televisions were priced at $5 each, then consumers would purchase them and probably buy more TVs than they need based on price. The demand will remain high. If the price is $50,000, this good would likely be considered a luxury good , and demand would be low.

Demand is the quantity of a good that consumers are willing and able to purchase at various prices at a given time.

This example assumes that product differentiation does not exist. There is only one type of product sold at a single price to every consumer. In this closed scenario, the item is not an essential human necessity such as food or shelter, does not have a substitute, and consumers expect prices to remain stable.

The supply curve considers the relationship between the price and available supply of an item from the producer's perspective rather than the consumer's.

When prices of a product increase, producers are willing to manufacture more of the product to realize greater profits. Falling prices depress production as producers may not recover input costs. If the costs to produce a TV are $50, production would be unprofitable when the selling price of the TV falls below $50.

If television prices are $1,000, manufacturers will focus on producing television sets over ventures and provide incentives to build more TVs. The behavior to seek maximum profits forces the supply curve to be upward-sloping.

An underlying assumption of the theory lies in the producer taking on the role of a price taker. Rather than dictating the prices of the product, this input is determined by the market, and suppliers only face the decision of how much to produce, given the market price. Optimal scenarios are not always the case, such as in monopolistic markets.

Consumers typically look for the lowest cost, and producers test their products at the highest price. When prices become unreasonable, consumers change their preferences and move away from the product.

A proper balance must be achieved where both parties engage in ongoing business transactions to benefit consumers and producers. In supply and demand theory, the optimal price that results in producers and consumers achieving the maximum combined utility occurs where the supply and demand lines intersect.

In What Types of Economies Are Laws of Supply and Demand Less Reliable?

If the economic environment is not a free market, supply and demand are not influential factors. In socialist economic systems , the government typically sets commodity prices regardless of the supply or demand conditions.

Does the Law of Supply and Demand Determine Market Conditions?

Multiple factors affect markets on both a microeconomic and a macroeconomic level. Supply and demand guide market behavior but do not determine it. Supply and demand are important factors, and Adam Smith referred to them as the invisible hand that guides a free market.

Does the Law of Supply and Demand Apply Only to Consumer Goods?

The theory of supply and demand relates not only to physical products such as television sets but also to wages and labor. More advanced theories of microeconomics and macroeconomics often adjust the assumptions and appearance of the supply and demand curve to illustrate concepts like economic surplus, monetary policy, aggregate supply and demand , fiscal stimulation, elasticity, and shortfalls.

The market theory of supply and demand was popularized by Adam Smith in 1776. Consumer demand for a good decreases as its price rises. As prices rise, producers manufacture more to gain more profits. The optimal price that shows an equilibrium between supply and demand is where the supply and demand lines intersect on a graph.

- A Practical Guide to Microeconomics 1 of 39

- Economists' Assumptions in Their Economic Models 2 of 39

- 5 Nobel Prize-Winning Economic Theories You Should Know About 3 of 39

- Positive vs. Normative Economics: What's the Difference? 4 of 39

- 5 Factors That Influence Competition in Microeconomics 5 of 39

- How Does Government Policy Impact Microeconomics? 6 of 39

- Microeconomics vs. Macroeconomics: What’s the Difference? 7 of 39

- How Do I Differentiate Between Micro and Macro Economics? 8 of 39

- Microeconomics vs. Macroeconomics Investments 9 of 39

- Introduction to Supply and Demand 10 of 39

- Is Demand or Supply More Important to the Economy? 11 of 39

- Demand: How It Works Plus Economic Determinants and the Demand Curve 12 of 39

- What Is the Law of Demand in Economics, and How Does It Work? 13 of 39

- Demand Curves: What Are They, Types, and Example 14 of 39

- Supply 15 of 39

- Law of Supply Explained, With the Curve, Types, and Examples 16 of 39

- Supply Curve: Definition, How It Works, and Example 17 of 39

- Elasticity: What It Means in Economics, Formula, and Examples 18 of 39

- Price Elasticity of Demand: Meaning, Types, and Factors That Impact It 19 of 39

- Elasticity vs. Inelasticity of Demand: What's the Difference? 20 of 39

- What Is Inelastic? Definition, Calculation, and Examples of Goods 21 of 39

- What Affects Demand Elasticity for Goods and Services? 22 of 39

- What Factors Influence a Change in Demand Elasticity? 23 of 39

- Utility in Economics Explained: Types and Measurement 24 of 39

- Utility in Microeconomics: Origins, Types, and Uses 25 of 39

- Utility Function Definition, Example, and Calculation 26 of 39

- Definition of Total Utility in Economics, With Example 27 of 39

- Marginal Utilities: Definition, Types, Examples, and History 28 of 39

- The Law of Diminishing Marginal Utility: How It Works, With Examples 29 of 39

- What Does the Law of Diminishing Marginal Utility Explain? 30 of 39

- Economic Equilibrium 31 of 39

- What Is the Income Effect? Its Meaning and Example 32 of 39

- Indifference Curves in Economics: What Do They Explain? 33 of 39

- Consumer Surplus Definition, Measurement, and Example 34 of 39

- What Is Comparative Advantage? 35 of 39

- What Are Economies of Scale? 36 of 39

- Perfect Competition: Examples and How It Works 37 of 39

- What Is the Invisible Hand in Economics? 38 of 39

- Market Failure: What It Is in Economics, Common Types, and Causes 39 of 39

:max_bytes(150000):strip_icc():format(webp)/DemandCurve-4197946-Final-64b129da426e4213a0911a47bb9a3bfa.jpg "demand economics assignment")

- Terms of Service

- Editorial Policy

- Privacy Policy

- Your Privacy Choices

The Law of Demand (With Diagram)

In this article we will discuss about:- 1. Introduction to the Law of Demand 2. Assumptions of the Law of Demand 3. Exceptions.

Introduction to the Law of Demand :

The law of demand expresses a relationship between the quantity demanded and its price. It may be defined in Marshall’s words as “the amount demanded increases with a fall in price, and diminishes with a rise in price”. Thus it expresses an inverse relation between price and demand. The law refers to the direction in which quantity demanded changes with a change in price.

On the figure, it is represented by the slope of the demand curve which is normally negative throughout its length. The inverse price- demand relationship is based on other things remaining equal. This phrase points towards certain important assumptions on which this law is based.

Assumptions of the Law of Demand:

These assumptions are:

ADVERTISEMENTS:

(i) There is no change in the tastes and preferences of the consumer;

(ii) The income of the consumer remains constant;

(iii) There is no change in customs;

(iv) The commodity to be used should not confer distinction on the consumer;

(v) There should not be any substitutes of the commodity;

(vi) There should not be any change in the prices of other products;

(vii) There should not be any possibility of change in the price of the product being used;

(viii) There should not be any change in the quality of the product; and

(ix) The habits of the consumers should remain unchanged. Given these conditions, the law of demand operates. If there is change even in one of these conditions, it will stop operating.

Given these assumptions, the law of demand is explained in terms of Table 3 and Figure 7.

What is Demand in Economics? Determinants, Types, Definition

- Post last modified: 6 April 2023

- Reading time: 40 mins read

- Post category: Economics

What is Demand in Economics?

Demand in Economics is an economic principle can be defined as the quantity of a product that a consumer desires to purchase goods and services at a specific price and time.

Factors such as the price of the product, the standard of living of people and change in customers’ preferences influence the demand. The demand for a product in the market is governed by the Laws of Economics

Table of Content

- 1 What is Demand in Economics?

- 2 Introduction to Demand in Economics

- 3 Meaning of Demand in Economics

- 4.1 To consider demand as an effective desire

- 4.2 Definition of demand in relation to price

- 4.3 Definition of Demand in relation to Price as well as Time

- 5 Demand Example

- 6.1 Price Demand

- 6.2 Income Demand

- 6.3 Cross Demand

- 6.4 Individual demand and Market demand

- 6.5 Joint Demand

- 6.6 Composite Demand

- 6.7 Direct and Derived Demand

- 7 Determinants of Demand

- 8.1 Importance in Consumption

- 8.2 Advantageous to producers

- 8.3 Importance in Exchange

- 8.4 Importance in Distribution

- 8.5 Importance in Public Finance

- 8.6 Importance of Law of Demand and Elasticity of Demand

- 8.7 Importance in Religion, Culture and Politics

- 9 Business Economics Tutorial

A market is a place where individuals, households, and businesses are engaged in the buying and selling of products and services through various modes.

The working of a market is governed by two forces, which are demand and supply . These two forces play a crucial role in determining the price of a product or service and size of the market.

Introduction to Demand in Economics

Demand in economics is a relationship between various possible prices of a product and the quantities purchased by the buyer at each price. In this relationship, price is an independent variable and the quantity demanded is the dependent variable.

In a market, the behavior of consumer can be analysed by using the concept of demand .

Also Read: What is Business Economics?

Meaning of Demand in Economics

In economics by demand , we mean the various quantities of a given good or service which buyer would purchase in one market during a given period of time, at various prices, or at various incomes, or at various prices of related goods.

Definition of Demand in Economics

We can divide the definitions of demand given by various economists into three Categories:

To consider demand as an effective desire

According to Person – “Demand implies three things

- desire to possess a thing

- means for purchasing it;

- willingness to use those means for purchasing.”

According to this definition there is no difference between demand and want, demand is considered as a synonym of want.

Definition of demand in relation to price

Some learned economists have expressed their views by co-relating demand with price.

Prof. Mill has expressed: “ We must mean by the word demand the quantity demanded and remember that this is not a fixed quantity but in general varies according to value. ”

In the, words of Waugh, “ The demand for any commodity is the relationship between the price and the quantity that will be purchased at that price. ”

Definition of Demand in relation to Price as well as Time

Mayers and Benham are worth mentioning economists who are of the view that demand is related, with both, price as well as time.

In the words of Mayers “ The demand for goods is a schedule of the amount that buyers would be willing to purchase at all possible prices at one instant of time. ”

According to Benham “ The demand for anything at a given price, is the amount of it which will be bought per unit of time at that price. ”

E ssentials of Demand

- To have an effective desire and ability to fulfil the desire and willingness to use those resources for fulfilment of the desire. It means consumer has a need and money to buy it.

- Demand for a particular commodity is related with a particular price for it;

- Demand for a particular commodity is related with per unit of time (daily, weekly, monthly, yearly etc.)

Also Read: What is Demand Schedule?

Demand Example

- Demand is always referred to in terms of price and bears no meaning if it is not expressed in relation to price. For example, an individual may be willing to purchase a shirt at a price of 500 but may not be willing to purchase the same shirt if it is valued at 1000. In addition, different quantities of a commodity are demanded at different prices.

- The quantity to be purchased

- The price at which the commodity is to be purchased

- The time period when the commodity is purchased

Also Read: What is Supply?

Types of Demand in Economics

7 Types of Demand in Economics are:

Price Demand

Income demand, cross demand, individual demand and market demand, joint demand, composite demand, direct and derived demand.

Price demand is a demand for different quantities of a product or service that consumers intend to purchase at a given price and time period assuming other factors, such as prices of the related goods, level of income of consumers, and consumer preferences, remain unchanged.

Price demand is inversely proportional to the price of a commodity or service. As the price of a commodity or service rises, its demand falls and vice versa.

Therefore, price demand indicates the functional relationship between the price of a commodity or service and the quantity demanded. It can be mathematically expressed as follows:

D A = f ( P A ) where, D A = Demand for commodity A f = Function P A =Price of commodity A

Income demand is a demand for different quantities of a commodity or service that consumers intend to purchase at different levels of income assuming other factors remain the same.

Generally, the demand for a commodity or service increases with an increase in the level of income of individuals except for inferior goods. Therefore, demand and income are directly proportional to normal goods whereas demand and income are inversely proportional to inferior goods.

The relationship between demand and income can be mathematically expressed as follows:

D A = f ( Y A ), where, D A = Demand for commodity A f = Function Y A = Income of consumer A

Cross demand is refers to the demand for different quantities of a commodity or service whose demand depends not only on its own price but also the price of other related commodities or services.

For example, tea and coffee are considered to be the substitutes of each other. Thus, when the price of coffee increases, people switch to tea. Consequently, the demand for tea increases. Thus, it can be said that tea and coffee have cross demand.

Mathematically, this can be expressed as follows:

D A = f (PB), where, D A = Demand for commodity A f = Function P B = Price of commodity B

Individual demand and market demand : This is the classification of demand based on the number of consumers in the market. In dividual demand refers to the quantity of a commodity or service demanded by an individual consumer at a given price at a given time period.

For example, the quantity of sugar that an individual or household purchases in a month is the individual or household demand. The individual demand of a product is influenced by the price of a product, the income of customers, and their tastes and preferences.

On the other hand, market demand is the aggregate of individual demands of all the consumers of a product over a period of time at a specific price while other factors are constant.

Joint demand is the quantity demanded two or more commodities or services that are used jointly and are, thus demanded together.

For example, car and petrol, bread and butter, pen and refill, etc. are commodities that are used jointly and are demanded together.

Composite demand is the demand for commodities or services that have multiple uses. For example, the demand for steel is a result of its use for various purposes like making utensils, car bodies, pipes, cans, etc.

For example, the demand for steel is a result of its use for various purposes like making utensils, car bodies, pipes, cans, etc. In the case of a commodity or service having composite demand, a change in price results in a large change in the demand. This is because the demand for the commodity or service would change across its various usages.

Direct and derived demand : Direct demand is the demand for commodities or services meant for final consumption. This demand arises out of the natural desire of an individual to consume a particular product.

For example, the demand for food, shelter, clothes, and vehicles is direct demand as it arises out of the biological, physical, and other personal needs of consumers.

On the other hand, derived demand refers to the demand for a product that arises due to the demand for other products.

For example, the demand for cotton to produce cotton fabrics is derived demand.

Also Read: Types of Demand in Economics

- Determinants of Demand

Determinants of demand are the factors that influence the decision of consumers to purchase a commodity or service.

- Price of a commodity : The price of a commodity or service is generally inversely proportional to the quantity demanded while other factors are constant.

- Price of related goods : The demand for a good or service not only depends on its own price but also on the price of related goods.

- Income of consumers : The level of income of individuals determines their purchasing power.

- Tastes and preferences of consumers : The demand for commodity changes with changes in the tastes and preferences of consumers

- Consumers expectations : Demand for commodities also depends on the consumers’ expectations regarding the future price of a commodity, availability of the commodity, changes in income.

- Credit policy : The credit policy of suppliers or banks also affects the demand for a commodity.

- Size and composition of the population : An increase in the size of a population increases the demand for commodities as the number of consumers would increase.

- Income distribution : Unequal distribution of income results in differences in the income status of different individuals in a nation.

- Climatic factors : The demand for commodities depends on the climatic conditions of a region such as cold, hot, humid, and dry.

- Government policy : Government policies have direct impact on the demand for various commodities.

Read Complete: 10 Determinants of Demand

Importance of Demand

Demand is considered the basis of the entire process of economic development, hence demand plays an important role in the economic, social and political fields.

The importance of demand are:

Importance in Consumption

Advantageous to producers, importance in exchange, importance in distribution, importance in public finance, importance of law of demand and elasticity of demand, importance in religion, culture and politics.

Demand implies the schedule of quantities to be purchased over a specific period of time at various prices. A consumer determines the quantity of various commodities to be consumed on the basis of his demand.

Producers maximize the profit by determining the nature, variety, quantity and cost of production on the basis of demand of various commodities and controlling the supply at an appropriate time.

Quantity demanded is the purchase of a commodity in certain quantity at a certain price, therefore it is exchanged. This means that production, purchase and sale of a particular commodity of a particular quality and quantity takes place in demand and it is the process of exchange.

Aggregate social production is determined on the basis of social demand. Production scale is increased with an increase in demand. Resources from various sources are procured to fulfill this increased demand. The share in the national product of a factor of production depends upon its demand.

Maximization of social welfare is the prime objective of the process of public finance. Sources of public revenue (inflows) and items of public expenditure (outflows) are determined to achieve this objective.

The Law of Demand and Elasticity of demand is the most important concept in economics.

Demand of various commodities in society at various points of time is also very important from the religious, cultural and political points of view. Efforts are made to fulfill the demand of various commodities that arises at the time of various social or religious festivals.

Also Read: What is Demand Function

- D N Dwivedi, Managerial Economics , 8th ed, Vikas Publishing House

- Petersen, Lewis & Jain, Managerial Economics , 4e, Pearson Education India

- Brigham, & Pappas, (1972). Managerial economics , 13ed. Hinsdale, Ill.: Dryden Press.

- Dean, J. (1951). Managerial economics (1st ed.). New York: Prentice-Hall.

Business Economics Tutorial

( Click on Topic to Read )

- What is Economics?

- Scope of Economics

- Nature of Economics

- What is Business Economics?

- Micro vs Macro Economics

- Laws of Economics

- Economic Statics and Dynamics

- Gross National Product (GNP)

- What is Business Cycle?

- W hat is Inflation?

- What is Demand?

- Types of Demand

- Determinants of Demand

- Law of Demand

- What is Demand Schedule?

- What is Demand Curve?

- What is Demand Function?

- Demand Curve Shifts

- What is Supply?

- Determinants of Supply

- Law of Supply

- What is Supply Schedule?

- What is Supply Curve?

Supply Curve Shifts

- What is Market Equilibrium?

Consumer Demand Analysis

- Consumer Demand

- Utility in Economics

- Law of Diminishing Marginal Utility

- Cardinal and Ordinal Utility

- Indifference Curve

- Marginal Rate of Substitution

- Budget Line

- Consumer Equilibrium

- Revealed Preference Theory

Elasticity of Demand & Supply

- Elasticity of Demand

- Price Elasticity of Demand

- Types of Price Elasticity of Demand

- Factors Affecting Price Elasticity of Demand

Importance of Price Elasticity of Demand

- Income Elasticity of Demand

- Cross Elasticity of Demand

- Advertisement Elasticity of Demand

- Elasticity of Supply

Cost & Production Analysis

- Production in Economics

- Production Possibility Curve

- Production Function

- Types of Production Functions

- Production in the Short Run

- Law of Diminishing Returns

- Isoquant Curve

- Producer Equilibrium

- Returns to Scale

Cost and Revenue Analysis

- Types of Cost

- Short Run Cost

- Long Run Cost

- Economies and Diseconomies of Scale

- What is Revenue?

Market Structure

- Types of Market Structures

- Profit Maximization

- What is Market Power?

- Demand Forecasting

- Methods of Demand Forecasting

- Criteria for Good Demand Forecasting

Market Failure

- What Market Failure?

Price Ceiling and Price Floor

Go On, Share article with Friends

Did we miss something in Business Economics Tutorial? Come on! Tell us what you think about our article on What is Demand | Business Economics in the comments section.

- What is Inflation?

You Might Also Like

What is advertisement elasticity of demand formula, example.

What is Utility in Economics? Definition, Meaning, Concept, Formula

What is a Production Possibility Curve? Definition, Example, Formula

What is Price Elasticity of Demand? Formula, Example, Measurement

What is Indifference Curve? Properties, Assumption, Analysis

What is marginal rate of substitution definition, formula.

What is Business Economics? Definition, Scope, Importance

What is market equilibrium definition, graph, price, demand & supply.

What is Economics? Definition, Meaning, Assumptions, Scope, Nature

Leave a reply cancel reply.

You must be logged in to post a comment.

World's Best Online Courses at One Place

We’ve spent the time in finding, so you can spend your time in learning

Digital Marketing

Personal growth.

Development

Faculty Resources

Assignments.

The assignments in this course are openly licensed, and are available as-is, or can be modified to suit your students’ needs. Answer keys are available to faculty who adopt Waymaker, OHM, or Candela courses with paid support from Lumen Learning. This approach helps us protect the academic integrity of these materials by ensuring they are shared only with authorized and institution-affiliated faculty and staff.

The assignments and discussion for this course align with the content and learning outcomes in each module. They will automatically be loaded into the assignment tool within your LMS. They can easily used as is, modified, or removed. You can preview them below.

Note that the Data Project Assignment is split into two parts and spans both module 6 and module 7. The Module 16 assignment presents two options, one that emphasizes topics from macroeconomics, and the other that emphasizes concepts from microeconomics.

- Assignments. Provided by : Lumen Learning. License : CC BY: Attribution

- Pencil Cup. Authored by : IconfactoryTeam. Provided by : Noun Project. Located at : https://thenounproject.com/term/pencil-cup/628840/ . License : CC BY: Attribution

- school Campus Bookshelves

- menu_book Bookshelves

- perm_media Learning Objects

- login Login

- how_to_reg Request Instructor Account

- hub Instructor Commons

- Download Page (PDF)

- Download Full Book (PDF)

- Periodic Table

- Physics Constants

- Scientific Calculator

- Reference & Cite

- Tools expand_more

- Readability

selected template will load here

This action is not available.

6.24: Assignment- Problem Set — Supply and Demand

- Last updated

- Save as PDF

- Page ID 60653

Click on the link to download the problem set for this module:

- Supply and Demand Problem Set

- Supply and Demand Problem Set. Provided by : Lumen Learning. License : CC BY: Attribution

Browse Course Material

Course info.

- Prof. Jonathan Gruber

Departments

As taught in.

- Microeconomics

Learning Resource Types

Principles of microeconomics, assignments.

You are leaving MIT OpenCourseWare

Changes in the wage rate (the price of labor) cause a movement along the demand curve. A change in anything else that affects demand for labor (e.g., changes in output, changes in the production process that use more or less labor, government regulation) causes a shift in the demand curve.

Changes in the wage rate (the price of labor) cause a movement along the supply curve. A change in anything else that affects supply of labor (e.g., changes in how desirable the job is perceived to be, government policy to promote training in the field) causes a shift in the supply curve.

Since a living wage is a suggested minimum wage, it acts like a price floor (assuming, of course, that it is followed). If the living wage is binding, it will cause an excess supply of labor at that wage rate.

Changes in the interest rate (i.e., the price of financial capital) cause a movement along the demand curve. A change in anything else (non-price variable) that affects demand for financial capital (e.g., changes in confidence about the future, changes in needs for borrowing) would shift the demand curve.

Changes in the interest rate (i.e., the price of financial capital) cause a movement along the supply curve. A change in anything else that affects the supply of financial capital (a non-price variable) such as income or future needs would shift the supply curve.

If market interest rates stay in their normal range, an interest rate limit of 35% would not be binding. If the equilibrium interest rate rose above 35%, the interest rate would be capped at that rate, and the quantity of loans would be lower than the equilibrium quantity, causing a shortage of loans.

b and c will lead to a fall in interest rates. At a lower demand, lenders will not be able to charge as much, and with more available lenders, competition for borrowers will drive rates down.

a and c will increase the quantity of loans. More people who want to borrow will result in more loans being given, as will more people who want to lend.

A price floor prevents a price from falling below a certain level, but has no effect on prices above that level. It will have its biggest effect in creating excess supply (as measured by the entire area inside the dotted lines on the graph, from D to S) if it is substantially above the equilibrium price. This is illustrated in the following figure.

It will have a lesser effect if it is slightly above the equilibrium price. This is illustrated in the next figure.

It will have no effect if it is set either slightly or substantially below the equilibrium price, since an equilibrium price above a price floor will not be affected by that price floor. The following figure illustrates these situations.

A price ceiling prevents a price from rising above a certain level, but has no effect on prices below that level. It will have its biggest effect in creating excess demand if it is substantially below the equilibrium price. The following figure illustrates these situations.

When the price ceiling is set substantially or slightly above the equilibrium price, it will have no effect on creating excess demand. The following figure illustrates these situations.

Neither. A shift in demand or supply means that at every price, either a greater or a lower quantity is demanded or supplied. A price floor does not shift a demand curve or a supply curve. However, if the price floor is set above the equilibrium, it will cause the quantity supplied on the supply curve to be greater than the quantity demanded on the demand curve, leading to excess supply.

Neither. A shift in demand or supply means that at every price, either a greater or a lower quantity is demanded or supplied. A price ceiling does not shift a demand curve or a supply curve. However, if the price ceiling is set below the equilibrium, it will cause the quantity demanded on the demand curve to be greater than the quantity supplied on the supply curve, leading to excess demand.

As an Amazon Associate we earn from qualifying purchases.

This book may not be used in the training of large language models or otherwise be ingested into large language models or generative AI offerings without OpenStax's permission.

Want to cite, share, or modify this book? This book uses the Creative Commons Attribution License and you must attribute OpenStax.

Access for free at https://openstax.org/books/principles-economics-2e/pages/1-introduction

- Authors: Steven A. Greenlaw, David Shapiro

- Publisher/website: OpenStax

- Book title: Principles of Economics 2e

- Publication date: Oct 11, 2017

- Location: Houston, Texas

- Book URL: https://openstax.org/books/principles-economics-2e/pages/1-introduction

- Section URL: https://openstax.org/books/principles-economics-2e/pages/chapter-4

© Jun 15, 2022 OpenStax. Textbook content produced by OpenStax is licensed under a Creative Commons Attribution License . The OpenStax name, OpenStax logo, OpenStax book covers, OpenStax CNX name, and OpenStax CNX logo are not subject to the Creative Commons license and may not be reproduced without the prior and express written consent of Rice University.

100+ Good Supply And Demand Economics Project Ideas

Supply and demand, among other economic concepts, are essential to our understanding of the world. You have undoubtedly learned about supply and demand economics project ideas in class if you are a student. It’s a basic idea that has far-reaching consequences in areas as diverse as the cost of your favorite snacks and the availability of jobs.

Taking up a supply and demand economics project is a fantastic approach to learning more about economics. This blog post will explain what a supply and demand economics project is, how to choose the best one and provide you with a list of over a hundred potential topics. We’ll talk about how these assignments help students in their learning, too.

You May Also Like: Finance And Economics Which One Is Better For Students Career

What Supply and Demand Economics Project Is?

Table of Contents

An economics supply and demand project is one in which the concepts of supply and demand are examined, researched, or put into practice. It helps students understand the dynamics of the market by bridging the gap between academic principles and real-world applications.

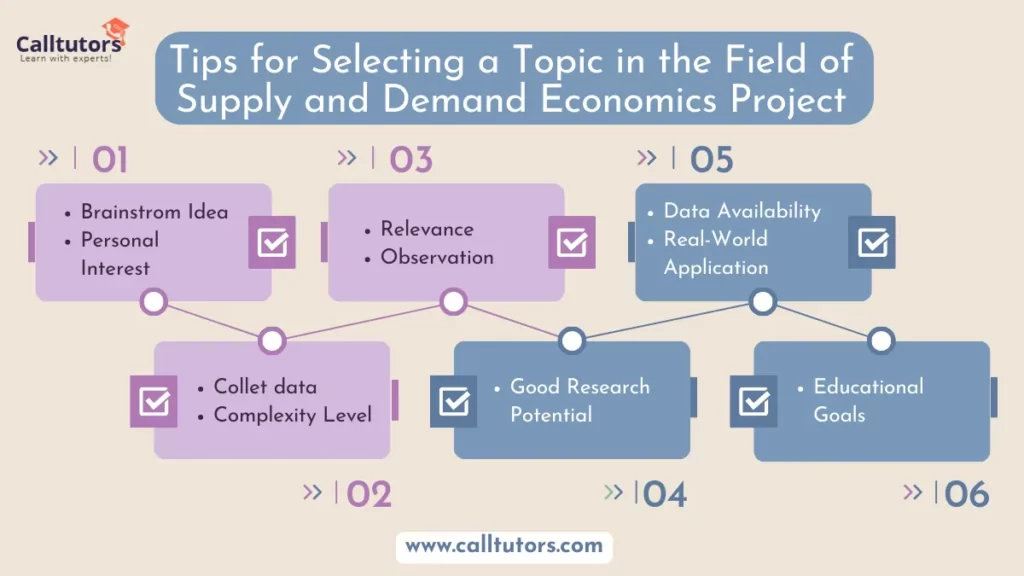

Tips for Selecting a Topic in the Field of Supply and Demand Economics Project

Choosing the correct supply and demand economics assignment will greatly enhance your educational experience. The perfect project for you may be found by following these guidelines.

1. Interest

Choose a project that you’d like to work on. Whether you’re researching the rise and fall of video game prices or the state of the employment market, a healthy dose of excitement goes a long way.

2. Relevance

Choose a project that has some kind of bearing on the actual world. Addressing problems you see or read about in the news might make for interesting and useful projects.

3. Complexity

Think about how well-versed you are in matters of complexity. If you’re a high school student just getting started with economics, it’s best to tackle easier assignments first.

4. Data Availability

The adequacy of available data for use in your project relies on your capacity to secure it. The availability of data is essential for doing useful studies.

5. Educational Goals

Consider what you want to achieve academically by working on this assignment. Is your goal to clarify an idea, forecast future events, or assess current tendencies?

Ideas for High School Economics Projects

The following list of categories contains over a hundred supply and demand economics project ideas.

1. Demand and Supply

- Examine the relationship between the asking price and sales of a well-liked video game.

- Determine whether there is a correlation between petrol prices and driving patterns.

- Determine whether there is a correlation between smartphone pricing and customer preferences.

2. Worker’s Market

- Look at how changes in the minimum wage affect the job market.

- Examine the impact of the employment market on the choice to go to college.

- Examine how many people are requesting aid from the government in proportion to the unemployment rate.

3. Buying Behaviour

- Look at what makes people choose organic over conventionally grown food.

- Consider the role of advertising and marketing in driving interest in certain goods or services.

- Examine how different income levels affect the desire for ostentatious purchases.

4. Market for Houses

- Look at how fluctuating interest rates affect the need for mortgage financing.

- Examine how the local rental market is affected by the current state of property prices.

- Find out what drives people to look for cheap homes.

5. Economics in a Sustainable World

- Learn more about how the demand for renewable energy is affected by carbon pricing regimes.

- Examine how electric car subsidies affect the demand for gas-powered automobiles.

- Learn more about the impact of laws and policies on the need for eco-friendly goods.

6. Agriculture and Food Systems

- Look at what influences consumers to choose organic over conventionally grown foods.

- Examine the impact of weather on crop supply and demand in agricultural economies.

- Find out how rising populations affect food supply and demand.

7. World Economy

- Examine how tariffs would affect the market for imported products in terms of both supply and demand.

- Consider the implications of a worldwide epidemic on distribution networks and the availability of goods.

- Find out what effect the fluctuating value of currencies has on international commerce.

8. Tools and Electronics

- Examine how the introduction of new smartphone models affects the demand for previous generations.

- Examine the effects on the availability and cost of electronic devices caused by interruptions in the supply chain.

- Check into the interest in paid streaming options.

9. Market for Energy

- Examine how OPEC’s policies affect oil prices and demand throughout the world.

- Examine how financial incentives for renewable energy sources have altered the market for green electricity.

- Examine how different climate patterns affect energy use.

Following are the best Supply And Demand Economics Project ideas for beginners, intermediate, and advanced level students.

Social Media Platforms

Sustainable and green economics, housing economics, tourism economics, transportation economics, luxury goods supply and demand economics project, art and collectibles, cryptocurrency economics, supply and demand economics project for political economics, sports economics, virtual economies supply and demand economics project, retail economics, agriculture and commodity markets, music industry economics, restaurant economics, fast food economics, pharmaceuticals and healthcare, social media economics, why these projects are beneficial for students.

Undertaking supply and demand economics projects offers numerous benefits to students:

- Real-World Application: These projects allow students to apply economic theories to real-world scenarios, enhancing their understanding of economic principles.

- Research and Analytical Skills: Students develop research and analytical skills by collecting and analyzing data related to supply and demand dynamics.

- Critical Thinking: These projects encourage critical thinking and problem-solving as students explore the cause-and-effect relationships in economic markets.

- Presentation Skills: Preparing and presenting the project findings helps students improve their communication skills.

- Relevance: Students gain insights into current economic issues and trends, making the subject matter more engaging and relevant.

- Preparation for Future Studies and Careers: Completing economics projects can prepare students for advanced studies in economics and future careers in fields like economics, business, finance, and public policy.

Economics Project Ideas

Now, let’s dive into 100+ supply and demand economics project ideas for students:

- 1. Price Elasticity of Demand for Gasoline: Analyze how consumers respond to changes in gasoline prices.

- 2. Impact of Advertising on Consumer Demand: Investigate how advertising affects the demand for products.

- 3. Supply and Demand for Smartphones: Examine how the release of a new smartphone impacts its price and demand.

- 4. The Economics of Fast Food: Study how fast food chains manage supply and demand.

- 5. Minimum Wage Effects: Research the effects of changes in the minimum wage on labor supply and demand.

- 6. Luxury vs. Necessity Goods: Compare the supply and demand for luxury goods with that of necessary items.

- 7. Real Estate Market Analysis: Investigate how factors like location, housing supply, and demand affect real estate prices.

Supply and demand economics projects offer an exciting and educational way for students to delve into the world of economics. With a wide array of project ideas available, students can choose topics that align with their interests, level of complexity, and the availability of data. These projects not only enhance students’ understanding of economic principles but also foster critical thinking, research skills, and an appreciation of how economics shapes the world around us.

Whether you’re a high school student looking for an engaging economics project or an educator seeking project ideas for your students, these suggestions provide a rich source of inspiration. By choosing a project that resonates with your interests, you can embark on an educational journey that combines theory with real-world applications, making economics come to life in a meaningful way.

Where can I find resources for my economics project?

You can find resources for your economics project in libraries, online databases, and academic websites. Additionally, your school or college may have resources available for research.

Are these projects suitable for high school students with no prior economics knowledge

Yes, these projects are designed to be accessible to students with various levels of knowledge.

What skills can I develop through supply and demand economics projects?

Supply and demand economics projects can help you develop research, critical thinking, data analysis, and presentation skills, among others.

Similar Articles

How To Do Homework Fast – 11 Tips To Do Homework Fast

Homework is one of the most important parts that have to be done by students. It has been around for…

How to Write an Assignment Introduction – 6 Best Tips

In essence, the writing tasks in academic tenure students are an integral part of any curriculum. Whether in high school,…

Leave a Comment Cancel Reply

Your email address will not be published. Required fields are marked *

This site uses Akismet to reduce spam. Learn how your comment data is processed .

IMAGES

VIDEO

COMMENTS

Demand is a description of all quantities of a good or service that a buyer would be willing to purchase at all prices. According to the law of demand, this relationship is always negative: the response to an increase in price is a decrease in the quantity demanded. For example, if the price of scented erasers decreases, buyers will respond to ...

Demand curves will be somewhat different for each product. They may appear relatively steep or flat, and they may be straight or curved. Nearly all demand curves share the fundamental similarity that they slope down from left to right, embodying the law of demand: As the price increases, the quantity demanded decreases, and, conversely, as the price decreases, the quantity demanded increases.

This chapter introduces the economic model of demand and supply—one of the most powerful models in all of economics. The discussion here begins by examining how demand and supply determine the price and the quantity sold in markets for goods and services, and how changes in demand and supply lead to changes in prices and quantities. Previous ...

Law Of Demand: The law of demand is a microeconomic law that states, all other factors being equal, as the price of a good or service increases, consumer demand for the good or service will ...

This 45-minute interactive lesson (in Google-Docs format) introduces the Law of Demand by engaging students with the media they use everyday, like our short instructional video on the demand curve. The Demand Curve. Watch on. But that's not the only way this lesson connects the demand curve to your students' lives: with current events, graphing ...

The law of supply and demand is a fundamental concept of economics and a theory popularized by Adam Smith in 1776. The principles of supply and demand are effective in predicting market behavior.

Unit 1: Supply and Demand. The first unit of this course is designed to introduce you to the principles of microeconomics and familiarize you with supply and demand diagrams, the most basic tool economists employ to analyze shifts in the economy. After completing this unit, you will be able to understand shifts in supply and demand and their ...

Preparation. The problem set is comprised of challenging questions that test your understanding of the material covered in the course. Make sure you have mastered the concepts and problem solving techniques from the following sessions before attempting the problem set: Introduction to Microeconomics. Applying Supply and Demand.

Some people supply it, and some people—you!—demand it. In this lecture, we will examine how to analyze supply and demand curves and the impact changes in market conditions and government policy can have on market equilibrium. Government intervention can impact gasoline prices. Image courtesy of Aaron Tyo-Dikerson on Flickr.

In this article we will discuss about:- 1. Introduction to the Law of Demand 2. Assumptions of the Law of Demand 3. Exceptions. Introduction to the Law of Demand: The law of demand expresses a relationship between the quantity demanded and its price. It may be defined in Marshall's words as "the amount demanded increases with a fall in price, and diminishes with a rise in price". Thus it ...

supply and demand, in economics, relationship between the quantity of a commodity that producers wish to sell at various prices and the quantity that consumers wish to buy. It is the main model of price determination used in economic theory. The price of a commodity is determined by the interaction of supply and demand in a market.The resulting price is referred to as the equilibrium price and ...

Demand in economics is a relationship between various possible prices of a product and the quantities purchased by the buyer at each price. In this relationship, price is an independent variable and the quantity demanded is the dependent variable. In a market, the behavior of consumer can be analysed by using the concept of demand.

Introduce the section. Step 2: PowerPoint ("Economics of Demand") Lecture - Section 3 Step 3: Show changes in graphs - give examples and have students graph the changes. Step 4: Assignment: Section 3 Worksheet. Day 4. Outcome: Students will create a demand schedule and a market demand curve for a specific product.

They can easily used as is, modified, or removed. You can preview them below. Note that the Data Project Assignment is split into two parts and spans both module 6 and module 7. The Module 16 assignment presents two options, one that emphasizes topics from macroeconomics, and the other that emphasizes concepts from microeconomics. Module.

After a few months into the product, the demand for the phone began to spiral downward. In here, D2 represents a decline in demand and D1 represents an increase shift in the demand. The company makes it money from the income that comes from the sales of this product. The only resolution to getting more money would be to lower the prices of ...

Book: Microeconomics (Lumen) 6: Module 3- Supply and Demand. Expand/collapse global location. 6.24: Assignment- Problem Set — Supply and Demand. Page ID. Table of contents. No headers. Click on the link to download the problem set for this module: Supply and Demand Problem Set.

Assignment demand and supply. Thanks.. Course. Introduction to Economics (ECON 1580) 845 Documents. ... Document (17) - Introduction to Economics ECON 1508 UNIT 2 ASSIGNMENT . Introduction to Economics. Assignments. 100% (13) 2. ECON1580 Discussion POST UNIT. 1. Introduction to Economics. Assignments. 100% (13) 12.

Problem Set 3 (PDF) Problem Set 4 (PDF) Problem Set 5 (PDF) Problem Set 6 Solutions (PDF) Problem Set 8 (PDF) Problem Set 9 Solutions (PDF) Problem Set 10 (PDF) Problem Set 10 Solutions (PDF) This section contains the problem sets and solutions for the course.

Introduction to Demand and Supply; 3.1 Demand, Supply, and Equilibrium in Markets for Goods and Services; 3.2 Shifts in Demand and Supply for Goods and Services; 3.3 Changes in Equilibrium Price and Quantity: The Four-Step Process; 3.4 Price Ceilings and Price Floors; 3.5 Demand, Supply, and Efficiency; Key Terms; Key Concepts and Summary; Self ...

Tips for Selecting a Topic in the Field of Supply and Demand Economics Project. Choosing the correct supply and demand economics assignment will greatly enhance your educational experience. The perfect project for you may be found by following these guidelines. 1. Interest. Choose a project that you'd like to work on.

In an economy, to fulfill all their needs, people demand goods and services. In economics, demand varies from want, wish, want and want. For productive demand, demand applies. A consumer who needs or wishes to supply a product or service must have the capacity to buy (purchasing power) and the willingness to pay for the said good or service.

To work as a Corporate Economist using your understanding of the Laws of Supply and Demand and Elasticity to successfully predict the impact of economic changes upon your company's production. impact of the hypothetical changes in Supply, Demand, and Elasticity indicated in the given chart of events. Role: You are an economist employed by a major corporation to predict the impact of economic ...

Grade 10 Economics P1 (English) November 2022 Question Paper- September 2023 Macroeconomics. Economics. Assignments. 96% (53) 6. EMS Controlled TEST QP Grade 9 TERM 1 2023. Economics. Assignments. 93% (140) 20. Grade 10 Economics P1 Macroeconomics (English) November 2022 Possible Answers - September 2023. Economics. Assignments. 91% (11) 4 ...

Economics document from Ethiopian Civil Service College, 37 pages, Great Land College MASTERS OF BUSINESS ADMINISTRATION Year I Second Semester Academic Year 2022/23 Individual Assignment For the Course of: Managerial Economics Submitted by:Temesgen Deressa: GLC/4035/15 Sec B Submitted to: Dr. Temesgen Furi July, 2023 Q