Want to create or adapt books like this? Learn more about how Pressbooks supports open publishing practices.

2.2 Components of the Strategic Planning Process

Learning objectives.

- Explain how a mission statement helps a company with its strategic planning.

- Describe how a firm analyzes its internal environment.

- Describe the external environment a firm may face and how it is analyzed.

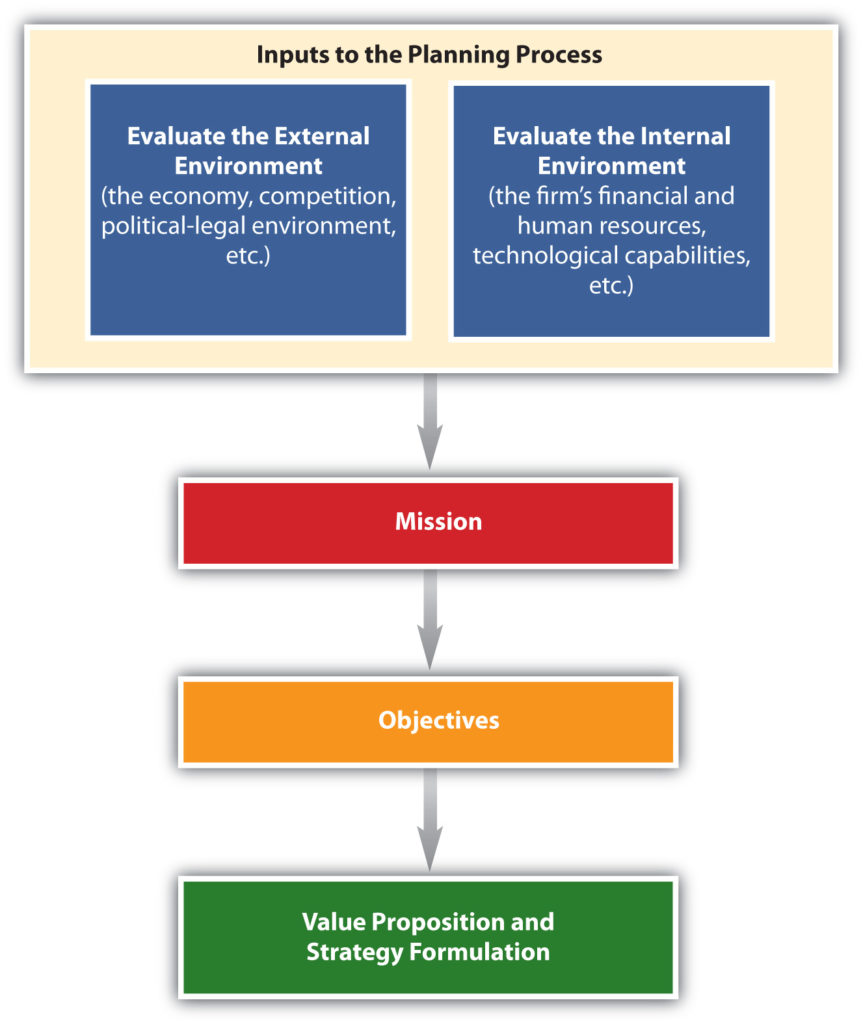

Strategic planning is a process that helps an organization allocate its resources to capitalize on opportunities in the marketplace. Typically, it is a long-term process. The strategic planning process includes conducting a situation analysis and developing the organization’s mission statement, objectives, value proposition, and strategies. Figure 2.2 “The Strategic Planning Process” shows the components of the strategic planning process. Let’s now look at each of these components.

Figure 2.2 The Strategic Planning Process

Conducting a Situation Analysis

As part of the strategic planning process, a situation analysis must be conducted before a company can decide on specific actions. A situation analysis involves analyzing both the external (macro and micro factors outside the organization) and the internal (company) environments. Figure 2.2 “The Strategic Planning Process” and Figure 2.3 “Elements of a SWOT Analysis” show examples of internal and external factors and in a SWOT analysis. The firm’s internal environment—such as its financial resources, technological resources, and the capabilities of its personnel and their performance—has to be examined. It is also critical to examine the external macro and micro environments the firm faces, such as the economy and its competitors. The external environment significantly affects the decisions a firm makes, and thus must be continuously evaluated. For example, during the economic downturn in 2008–2009, businesses found that many competitors cut the prices of their products drastically. Other companies reduced package sizes or the amount of product in packages. Firms also offered customers incentives (free shipping, free gift cards with purchase, rebates, etc.) to purchase their goods and services online, which allowed businesses to cut back on the personnel needed to staff their brick-and-mortar stores. While a business cannot control things such as the economy, changes in demographic trends, or what competitors do, it must decide what actions to take to remain competitive—actions that depend in part on their internal environment.

Conducting a SWOT Analysis

Based on the situation analysis, organizations analyze their s trengths, w eaknesses, o pportunities, and t hreats, or conduct what’s called a SWOT analysis . Strengths and weaknesses are internal factors and are somewhat controllable. For example, an organization’s strengths might include its brand name, efficient distribution network, reputation for great service, and strong financial position. A firm’s weaknesses might include lack of awareness of its products in the marketplace, a lack of human resources talent, and a poor location. Opportunities and threats are factors that are external to the firm and largely uncontrollable. Opportunities might entail the international demand for the type of products the firm makes, few competitors, and favorable social trends such as people living longer. Threats might include a bad economy, high interest rates that increase a firm’s borrowing costs, and an aging population that makes it hard for the business to find workers.

You can conduct a SWOT analysis of yourself to help determine your competitive advantage. Perhaps your strengths include strong leadership abilities and communication skills, whereas your weaknesses include a lack of organization. Opportunities for you might exist in specific careers and industries; however, the economy and other people competing for the same position might be threats. Moreover, a factor that is a strength for one person (say, strong accounting skills) might be a weakness for another person (poor accounting skills). The same is true for businesses. See Figure 2.3 “Elements of a SWOT Analysis” for an illustration of some of the factors examined in a SWOT analysis.

Figure 2.3 Elements of a SWOT Analysis

The easiest way to determine if a factor is external or internal is to take away the company, organization, or individual and see if the factor still exists. Internal factors such as strengths and weaknesses are specific to a company or individual, whereas external factors such as opportunities and threats affect multiple individuals and organizations in the marketplace. For example, if you are doing a situation analysis on PepsiCo and are looking at the weak economy, take PepsiCo out of the picture and see what factors remain. If the factor—the weak economy—is still there, it is an external factor. Even if PepsiCo hadn’t been around in 2008–2009, the weak economy reduced consumer spending and affected a lot of companies.

Assessing the Internal Environment

As we have indicated, when an organization evaluates which factors are its strengths and weaknesses, it is assessing its internal environment. Once companies determine their strengths, they can use those strengths to capitalize on opportunities and develop their competitive advantage. For example, strengths for PepsiCo are what are called “mega” brands, or brands that individually generate over $1 billion in sales 1 . These brands are also designed to contribute to PepsiCo’s environmental and social responsibilities.

PepsiCo’s brand awareness, profitability, and strong presence in global markets are also strengths. Especially in foreign markets, the loyalty of a firm’s employees can be a major strength, which can provide it with a competitive advantage. Loyal and knowledgeable employees are easier to train and tend to develop better relationships with customers. This helps organizations pursue more opportunities.

Although the brand awareness for PepsiCo’s products is strong, smaller companies often struggle with weaknesses such as low brand awareness, low financial reserves, and poor locations. When organizations assess their internal environments, they must look at factors such as performance and costs as well as brand awareness and location. Managers need to examine both the past and current strategies of their firms and determine what strategies succeeded and which ones failed. This helps a company plan its future actions and improves the odds they will be successful. For example, a company might look at packaging that worked very well for a product and use the same type of packaging for new products. Firms may also look at customers’ reactions to changes in products, including packaging, to see what works and doesn’t work. When PepsiCo changed the packaging of major brands in 2008, customers had mixed responses. Tropicana switched from the familiar orange with the straw in it to a new package and customers did not like it. As a result, Tropicana changed back to their familiar orange with a straw after spending $35 million for the new package design.

Tropicana’s Recent Ad

(click to see video)

Tropicana’s recent ad left out the familiar orange with a straw.

Individuals are also wise to look at the strategies they have tried in the past to see which ones failed and which ones succeeded. Have you ever done poorly on an exam? Was it the instructor’s fault, the strategy you used to study, or did you decide not to study? See which strategies work best for you and perhaps try the same type of strategies for future exams. If a strategy did not work, see what went wrong and change it. Doing so is similar to what organizations do when they analyze their internal environments.

Assessing the External Environment

Analyzing the external environment involves tracking conditions in the macro and micro marketplace that, although largely uncontrollable, affect the way an organization does business. The macro environment includes economic factors, demographic trends, cultural and social trends, political and legal regulations, technological changes, and the price and availability of natural resources. Each factor in the macro environment is discussed separately in the next section. The micro environment includes competition, suppliers, marketing intermediaries (retailers, wholesalers), the public, the company, and customers. We focus on competition in our discussion of the external environment in the chapter. Customers, including the public will be the focus of Chapter 3 “Consumer Behavior: How People Make Buying Decisions” and marketing intermediaries and suppliers will be discussed in Chapter 8 “Using Marketing Channels to Create Value for Customers” and Chapter 9 “Using Supply Chains to Create Value for Customers” .

When firms globalize, analyzing the environment becomes more complex because they must examine the external environment in each country in which they do business. Regulations, competitors, technological development, and the economy may be different in each country and will affect how firms do business. To see how factors in the external environment such as technology may change education and lives of people around the world, watch the videos “Did You Know 2.0?” and “Did You Know 3.0?” which provide information on social media sites compared to populations in the world. Originally created in 2006 and revised in 2007, the video has been updated and translated into other languages. Another edition of “Did You Know?” (4.0) focused on changing media and technology and showed how information may change the world as well as the way people communicate and conduct business.

Did You Know 2.0?

To see how the external environment and world are changing and in turn affecting marketing strategies, check out “Did You Know 2.0?”

Did You Know 4.0?

To see how fast things change and the impact of technology and social media, visit “Did You Know 4.0?”

Although the external environment affects all organizations, companies must focus on factors that are relevant for their operations. For example, government regulations on food packaging will affect PepsiCo but not Goodyear. Similarly, students getting a business degree don’t need to focus on job opportunities for registered nurses.

The Competitive Environment

All organizations must consider their competition, whether it is direct or indirect competition vying for the consumer’s dollar. Both nonprofit and for-profit organizations compete for customers’ resources. Coke and Pepsi are direct competitors in the soft drink industry, Hilton and Sheraton are competitors in the hospitality industry, and organizations such as United Way and the American Cancer Society compete for resources in the nonprofit sector. However, hotels must also consider other options that people have when selecting a place to stay, such as hostels, dorms, bed and breakfasts, or rental homes.

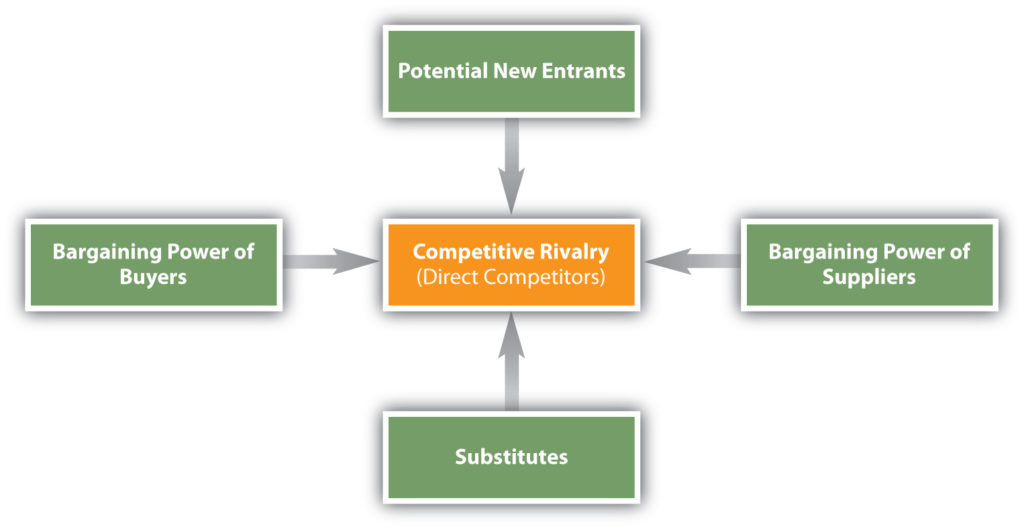

A group of competitors that provide similar products or services form an industry. Michael Porter, a professor at Harvard University and a leading authority on competitive strategy, developed an approach for analyzing industries. Called the five forces model (Porter, 1980) and shown in Figure 2.5 “Five Forces Model” , the framework helps organizations understand their current competitors as well as organizations that could become competitors in the future. As such, firms can find the best way to defend their position in the industry.

Figure 2.5 Five Forces Model (Porter, 1980)

Competitive Analysis

When a firm conducts a competitive analysis, they tend to focus on direct competitors and try to determine a firm’s strengths and weaknesses, its image, and its resources. Doing so helps the firm figure out how much money a competitor may be able to spend on things such as research, new product development, promotion, and new locations. Competitive analysis involves looking at any information (annual reports, financial statements, news stories, observation details obtained on visits, etc.) available on competitors. Another means of collecting competitive information utilizes mystery shoppers , or people who act like customers. Mystery shoppers might visit competitors to learn about their customer service and their products. Imagine going to a competitor’s restaurant and studying the menu and the prices and watching customers to see what items are popular and then changing your menu to better compete. Competitors battle for the customer’s dollar and they must know what other firms are doing. Individuals and teams also compete for jobs, titles, and prizes and must figure out the competitors’ weaknesses and plans in order to take advantage of their strengths and have a better chance of winning.

According to Porter, in addition to their direct competitors (competitive rivals), organizations must consider the strength and impact the following could have (Porter, 1980):

- Substitute products

- Potential entrants (new competitors) in the marketplace

- The bargaining power of suppliers

- The bargaining power of buyers

When any of these factors change, companies may have to respond by changing their strategies. For example, because buyers are consuming fewer soft drinks these days, companies such as Coke and Pepsi have had to develop new, substitute offerings such as vitamin water and sports drinks. However, other companies such as Dannon or Nestlé may also be potential entrants in the flavored water market. When you select a hamburger fast-food chain, you also had the option of substitutes such as getting food at the grocery or going to a pizza place. When computers entered the market, they were a substitute for typewriters. Most students may not have ever used a typewriter, but some consumers still use typewriters for forms and letters.

When personal computers were first invented, they were a serious threat to typewriter makers such as Smith Corona.

mpclemens – Smith-Corona Classic 12 – CC BY 2.0.

Suppliers, the companies that supply ingredients as well as packaging materials to other companies, must also be considered. If a company cannot get the supplies it needs, it’s in trouble. Also, sometimes suppliers see how lucrative their customers’ markets are and decide to enter them. Buyers, who are the focus of marketing and strategic plans, must also be considered because they have bargaining power and must be satisfied. If a buyer is large enough, and doesn’t purchase a product or service, it can affect a selling company’s performance. Walmart, for instance, is a buyer with a great deal of bargaining power. Firms that do business with Walmart must be prepared to make concessions to them if they want their products on the company’s store shelves.

Lastly, the world is becoming “smaller” and a more of a global marketplace. Companies everywhere are finding that no matter what they make, numerous firms around the world are producing the same “widget” or a similar offering (substitute) and are eager to compete with them. Employees are in the same position. The Internet has made it easier than ever for customers to find products and services and for workers to find the best jobs available, even if they are abroad. Companies are also acquiring foreign firms. These factors all have an effect on the strategic decisions companies make.

The Political and Legal Environment

All organizations must comply with government regulations and understand the political and legal environments in which they do business. Different government agencies enforce the numerous regulations that have been established to protect both consumers and businesses. For example, the Sherman Act (1890) prohibits U.S. firms from restraining trade by creating monopolies and cartels. The regulations related to the act are enforced by the Federal Trade Commission (FTC), which also regulates deceptive advertising. The U.S. Food and Drug Administration (FDA) regulates the labeling of consumable products, such as food and medicine. One organization that has been extremely busy is the Consumer Product Safety Commission, the group that sets safety standards for consumer products. Unsafe baby formula and toys with lead paint caused a big scare among consumers in 2008 and 2009.

The U.S. Food and Drug Administration prohibits companies from using unacceptable levels of lead in toys and other household objects, such as utensils and furniture. Mattel voluntarily recalled Sarge cars made in mid-2000.

U.S. Consumer Product Safety Commission – public domain.

As we have explained, when organizations conduct business in multiple markets, they must understand that regulations vary across countries and across states. Many states and countries have different laws that affect strategy. For example, suppose you are opening up a new factory because you cannot keep up with the demand for your products. If you are considering opening the factory in France (perhaps because the demand in Europe for your product is strong), you need to know that it is illegal for employees in that country to work more than thirty-five hours per week.

The Economic Environment

The economy has a major impact on spending by both consumers and businesses, which, in turn, affects the goals and strategies of organizations. Economic factors include variables such as inflation, unemployment, interest rates, and whether the economy is in a growth period or a recession. Inflation occurs when the cost of living continues to rise, eroding the purchasing power of money. When this happens, you and other consumers and businesses need more money to purchase goods and services. Interest rates often rise when inflation rises. Recessions can also occur when inflation rises because higher prices sometimes cause low or negative growth in the economy.

During a recessionary period, it is possible for both high-end and low-end products to sell well. Consumers who can afford luxury goods may continue to buy them, while consumers with lower incomes tend to become more value conscious. Other goods and services, such as products sold in traditional department stores, may suffer. In the face of a severe economic downturn, even the sales of luxury goods can suffer. The economic downturn that began in 2008 affected consumers and businesses at all levels worldwide. Consumers reduced their spending, holiday sales dropped, financial institutions went bankrupt, the mortgage industry collapsed, and the “Big Three” U.S. auto manufacturers (Ford, Chrysler, and General Motors) asked for emergency loans.

The demographic and social and cultural environments—including social trends, such as people’s attitudes toward fitness and nutrition; demographic characteristics, such as people’s age, income, marital status, education, and occupation; and culture, which relates to people’s beliefs and values—are constantly changing in the global marketplace. Fitness, nutrition, and health trends affect the product offerings of many firms. For example, PepsiCo produces vitamin water and sports drinks. More women are working, which has led to a rise in the demand for services such as house cleaning and daycare. U.S. baby boomers are reaching retirement age, sending their children to college, and trying to care of their elderly parents all at the same time. Firms are responding to the time constraints their buyers face by creating products that are more convenient, such as frozen meals and nutritious snacks.

The composition of the population is also constantly changing. Hispanics are the fastest-growing minority in the United States. Consumers in this group and other diverse groups prefer different types of products and brands. In many cities, stores cater specifically to Hispanic customers.

The technology available in the world is changing the way people communicate and the way firms do business. Everyone is affected by technological changes. Self-scanners and video displays at stores, ATMs, the Internet, and mobile phones are a few examples of how technology is affecting businesses and consumers. Many consumers get information, read the news, use text messaging, and shop online. As a result, marketers have begun allocating more of their promotion budgets to online ads and mobile marketing and not just to traditional print media such as newspapers and magazines. Applications for telephones and electronic devices are changing the way people obtain information and shop, allowing customers to comparison shop without having to visit multiple stores. As you saw in “Did You Know 4.0?” technology and social media are changing people’s lives. Many young people may rely more on electronic books, magazines, and newspapers and depend on mobile devices for most of their information needs. Organizations must adapt to new technologies in order to succeed.

Technology changes the way we do business. Banking on a cell phone adds convenience for customers. Bar codes on merchandise speed the checkout process.

first direct – first direct Banking ‘on the go’ iPhone App – front – CC BY-NC-ND 2.0; Paul Domenick – Lasered – CC BY-NC-ND 2.0.

Natural Resources

Natural resources are scarce commodities, and consumers are becoming increasingly aware of this fact. Today, many firms are doing more to engage in “sustainable” practices that help protect the environment and conserve natural resources. Green marketing involves marketing environmentally safe products and services in a way that is good for the environment. Water shortages often occur in the summer months, so many restaurants now only serve patrons water upon request. Hotels voluntarily conserve water by not washing guests’ sheets and towels every day unless they request it. Reusing packages (refillable containers) and reducing the amount of packaging, paper, energy, and water in the production of goods and services are becoming key considerations for many organizations, whether they sell their products to other businesses or to final users (consumers). Construction companies are using more energy efficient materials and often have to comply with green building solutions. Green marketing not only helps the environment but also saves the company, and ultimately the consumer, money. Sustainability, ethics (doing the right things), and social responsibility (helping society, communities, and other people) influence an organization’s planning process and the strategies they implement.

Although environmental conditions change and must be monitored continuously, the situation analysis is a critical input to an organization’s or an individual’s strategic plan. Let’s look at the other components of the strategic planning process.

The Mission Statement

The firm’s mission statement states the purpose of the organization and why it exists. Both profit and nonprofit organizations have mission statements, which they often publicize. The following are examples of mission statements:

PepsiCo’s Mission Statement “Our mission is to be the world’s premier consumer products company focused on convenient foods and beverages. We seek to produce financial rewards to investors as we provide opportunities for growth and enrichment to our employees, our business partners and the communities in which we operate. And in everything we do, we strive for honesty, fairness and integrity 2 .” The United Way’s Mission Statement “To improve lives by mobilizing the caring power of communities 3 .”

Sometimes SBUs develop separate mission statements. For example, PepsiCo Americas Beverages, PepsiCo Americas Foods, and PepsiCo International might each develop a different mission statement.

Key Takeaway

A firm must analyze factors in the external and internal environments it faces throughout the strategic planning process. These factors are inputs to the planning process. As they change, the company must be prepared to adjust its plans. Different factors are relevant for different companies. Once a company has analyzed its internal and external environments, managers can begin to decide which strategies are best, given the firm’s mission statement.

Review Questions

- What factors in the external environment are affecting the “Big Three” U.S. automobile manufacturers?

- What are some examples of Walmart’s strengths?

- Suppose you work for a major hotel chain. Using Porter’s five forces model, explain what you need to consider with regard to each force.

1 PepsiCo, Inc., “PepsiCo Brands,” http://www.pepsico.com/Company/Our-Brands.html (accessed December 7, 2009).

2 PepsiCo, Inc., “Our Mission and Vision,” http://www.pepsico.com/Company/Our-Mission-and-Vision.html (accessed December 7, 2009).

3 United Way Worldwide, “Mission and Vision,” http://www.liveunited.org/about/missvis.cfm (accessed December 7, 2009).

Principles of Marketing Copyright © 2015 by University of Minnesota is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License , except where otherwise noted.

Share This Book

The Skyline G Blog: New ideas and perspectives focused on results

What is Strategic Planning? The Key Components, Process & Role Leaders Play in Ensuring a Strategy's Success

by Thuy Sindell, PhD. and Milo Sindell, MS.

Strategic planning is a process that is essential for companies to ensure successful and sustainable growth.

An intelligent and actionable strategic plan is a vital part of competing within the marketplace. It directs businesses to take meaningful action to help them reach their organization’s goals by mapping out a clear direction, creating measurable goals, and allocating resources to pursue these specific objectives.

What is Strategic Planning?

A strategic plan is an essential process and strategy execution document for any company looking to make the most of its resources and reach long-term organizational goals.

This vital and continually evolving document outlines a clear direction, sets objectives that must be achieved, and provides an actionable roadmap for success; it also helps organizations stand out from competitors by allowing them to differentiate themselves in the marketplace with their unique approach.

A well-crafted strategic plan will help companies stay focused on their mission while making decisions based on core values guiding them toward achieving desired results by ensuring everyone is moving in the same direction.

What are the Key Components of a Strategic Plan?

Several key components make up a well-developed strategic plan. These key components include:

A Mission Statement

An organization’s mission statement states the company’s purpose and the reasons why it exists. Although you might be already clear on the mission, reiterating your mission statement and connection to the plan acts as a foundation for the strategic plan and your strategy.

A Vision Statement

The company vision is the bigger objective that the company aspires to achieve. This may be as broad as making the world a better place through your product or service or ridding bathrooms of mildew. Whatever your vision, it should be connected to your strategic plan

Aligning the company mission and vision statements is the first crucial step to strategic planning.

SWOT Analysis

An overall evaluation of the company’s strengths, weaknesses, opportunities, and threats. Knowing these points will help you leverage your resources, shore up gaps, and realistically plan your path and the potential risks. Your SWOT analysis will help ensure that your strategic plan is based upon reality and play an important part in your strategic management process.

Goals & Objectives

Goals and objectives need specific, measurable, achievable, and time-bound targets the company wants to achieve. Ensure your goals are achievable, measurable, and can be clearly communicated as part of your strategic planning. High-level company objectives should cascade and align with the objectives of various divisions and teams. The Strategic plans of each division and team should map directly to broader company goals and methods.

The specific courses of action that the company will take to achieve its measurable goals and specific strategic issues.

Action Plans

Detailed project plans outlining the specific steps that will be taken to implement the strategies.

Resource Allocation

The allocation of financial, human, and other resources to implement the action plans.

Evaluation and Control

Evaluation and control are based on measures and systems to monitor the company’s progress toward achieving its organization’s goals, objectives, and financial plan and to make adjustments as necessary.

Who is Responsible for Creating a Strategic Plan?

In general, creating a strategic plan is the responsibility of the company’s top management team - the CEO, CFO, other executives, etc.

However, though the top management will do the strategic thinking, it’s essential for key members throughout the entire organization to be involved in the strategic planning process as different departments, employees, and human resources will have valuable insights and perspectives to contribute to the strategy formation. Also, when various constituents are a part of and the planning process a sense of ownership and commitment to the strategic plan’s success is reinforced.

It’s also common for companies to seek input from external stakeholders, customers, suppliers, and industry experts as part of the strategic planning process. As part of your planning process make sure to identify any critical stakeholders outside of your company.

What Makes the Strategic Planning Process Effective?

Below are some key factors that contribute to the overall effectiveness of a successful strategic plan and the strategic planning process. Understanding these points will help make your strategic planning process more effective:

The plan needs to be clear & concise, with specific strategic goals & objectives that are easy for everyone to understand. Senior leadership plays a critical role in ensuring that each objective is clear and how objectives will be achieved is understood.

The strategic plan needs to take the company’s resources & capabilities into account, and the goals need to be realistic & achievable based on the market data.

The plan needs to be flexible enough to allow for adjustments to be made in response to changes in the external environment after deployment.

The plan must be aligned with the company’s mission, vision & values and should support the organization’s overall direction in terms of business plan and annual budgets.

Easily Communicated

The plan needs to be communicated effectively to all stakeholders & investors, including employees & customers.

The plan needs clear & actionable steps and a timeline for implementation. It must be followed consistently to ensure progress toward business goals like increasing sales and maximizing profit.

The plan needs to measure & evaluate progress, collect feedback, and be reviewed and updated regularly to ensure continuous progress toward company goals and that the plan remains relevant and practical and targets logical key performance indicators.

An effective strategic plan identifies potential factors that might derail the plan and, at a minimum, provides high-level alternatives should the plan become derailed.

When Do Strategic Plans Fail?

Listed below are a few potential reasons why strategic planning might fail. Understanding why strategic plans fail will help create more effective strategic planning outcomes:

Lacks Clarity

Plans need to be clear and specific. If not, it may be difficult to understand and challenging to implement. When a strategic plan is ambitious it is tough for people to feel connected and motivated to take action.

Lack of Realistic Options and Objectives

Plans need to be realistic. If the plan cannot really be achieved, it’ll be difficult to implement and lead to frustration, disappointment, and potential failure.

Lack of Flexibility

The plan needs to be flexible; if it’s not is not flexible and doesn’t allow for adjustments in response to changes in the environment (internal and external) or from evaluation or measurement, it may become irrelevant or ineffective.

Lack of Alignment

The plan needs to be aligned with the company’s mission, vision, and values; if not consistent with the organization’s overall direction, it can quickly become out of sync with its underlying purpose and be ineffective in helping to reach desired goals.

Lack of Understanding

The plan needs to be communicated effectively to all key stakeholders and take feedback from all stakeholders; otherwise, it may be misunderstood or, worse - ignored or seen as not valuable.

Lack Actionable Steps

The strategic plan needs to be implemented swiftly and consistently; if the action steps are not clear or too hard to implement, they may not be implemented effectively.

Lack of Measurable Outcomes

The strategic plan needs to be reviewed and updated regularly, and its performance evaluated after implementation; otherwise, it may become ineffective or outdated, therefore ineffective at achieving desired outcomes.

External Factors

Changes in the external environment can have a huge effect. Changes like shifts in the economy or customer preferences, if not accounted for, can seriously impact the effectiveness of a once brilliant strategic plan.

However, as in life and business, things change, and every business must be able to adapt quickly to changing circumstances. This is why an effective plan includes contingencies.

What is a Company Leader’s Role in Ensuring the Strategic Plan is Implemented Successfully?

Strategic management.

Company leaders are responsible for ensuring that the strategic plan is implemented successfully.

Some specific ways business leaders can ensure the plan is implemented properly are:

Clearly Communicate the Plan

Business leaders need to communicate the strategic plan effectively to all key stakeholders, including employees, customers, and investors. Any questions need to be answered and clarified, so everyone is aligned. The strategic plan should be shared in a way that you (the leader) demonstrate ownership and enthusiasm and can share with your team how each role is vital to achieving the plan’s objectives.

Providing Resources

Leaders need to ensure that resources, such as funding, personnel, and technology, are available to everyone needed in order to implement the plan successfully.

Setting Expectations

Leaders need to set clear expectations for implementing the plan and hold the designated employees accountable for meeting those expectations. Clear and achievable timelines need to be established and committed to by each stakeholder.

Leading by Example

Leaders need to model the behaviors and values outlined in the plan and encourage others to do the same.

Providing Support

Leaders need to provide support and guidance to employees as they work through problems toward achieving the strategic goals and objectives of the plan.

Monitoring Progress

Leaders need to monitor the progress towards achieving the goals and objectives outlined in the plan and make adjustments in the operational plans as they see fit, as needed.

Celebrating Successes

Leaders need to recognize and celebrate wins along the way to help keep morale high and encourage continued progress toward the ultimate goals.

What’s the Role of Each Individual Employee in Implementing & Supporting the Strategic Plans Success?

Employees are the driving force and critical in implementing and supporting the strategic plan’s success. Your employees will be the eyes and ears of how the strategic plan works. This is why it is vital for leaders to create a business environment where there is open communication and all types of information can be shared and reviewed in relation to its impact on the long- term strategy. Leaders must foster an open environment where questions can be asked and bad and good news shared. Leaders can help employees play their part by ensuring employees are supported and are clear on their ability to do the following:

Understand the Plan

Employees need to understand the strategic plan, how it aligns with the company’s mission, the steps to take, and most importantly, the goals.

Aligning Work and Job Goals with the Plan

Leaders, managers, and employees need to align their work with the strategic plan and prioritize tasks that support achieving the plan’s goals & strategic objectives.

Manage Implementation

Employees must consistently follow through on their assigned tasks and responsibilities to implement the plans, steps, and processes.

Provide Feedback

During the initial review of the organization’s current status, employees must provide feedback and suggestions to improve the plan. During its implementation, employees need to provide feedback based on performance and potentially adjust the plan if needed for better performance and goals.

Communicate Laterally and Up

Employees need to communicate with coworkers to ensure everyone is working towards the same goals & objectives and, most importantly, employees need to communicate to their manager on how their contribution is proceeding.

Seek Support and Guidance

Employees need to seek support and guidance from leaders if they need help implementing any steps of the plan or achieving goals.

Do Some Companies Believe that Strategic Planning is a Waste of Time?

Sure. It’s possible some companies may view strategic planning as a waste of time. This could be due to a variety of reasons: resources required upfront, lack of understanding of the benefits of strategic planning, a lack of buy-in from senior management, or a lack of resources to dedicate to the process.

However, for massively successful companies, strategic planning is recognized as an invaluable tool to help organizations achieve their long-term goals and be outstanding in a competitive marketplace.

Strategic planning can also help companies be more agile and adapt to changes in the external environment. For these reasons, it’s generally recommended that companies engage in strategic planning and review results on a regular basis.

What Makes a Great Strategy?

What makes a great competitive strategy? Several characteristics are often considered to be key elements of great strategy execution:

A great strategy is clear & easy to understand, with specific goals & strategic objectives that are well-defined.

A great strategy is a focused strategy. A great strategy is focused on a specific area of the business and doesn’t try to do too many things at once.

A great strategy is aligned with the company’s overall mission, vision for the future, and values, supporting the organization’s overall direction.

Flexibility

A great strategy is flexible and allows for adjustments to be made in response to results and changes in the external environment.

A great strategy is realistic & achievable, taking into account the company’s resources & capabilities and what can actually get done.

Differentiation

The great strategy sets the company apart from its competitors in the marketplace and helps it to differentiate itself from competitors to customers.

A great strategy can be executed effectively, with clear action steps, a timeline for implementation, and who is responsible for each action step.

Evaluation & Feedback

The great strategy includes measures for evaluating progress and collecting feedback, and it needs to be reviewed regularly & potentially updated to ensure it remains relevant & effective.

When is a Great Strategy Not Enough to Ensure Company Success?

While a great strategy can certainly be a key factor in a company’s success, it’s not the only factor needed to be successful. There are a number of other internal and external factors that can impact a company’s success, including:

Even the best strategy will not be a successful strategy if executed poorly.

A company needs resources, period. Resources like funding, personnel, and technology, are essential to implement strategy effectively.

Changes in external factors are equally important as the internal environment. For example, economic shifts or customer preferences can impact a company’s success.

Competition

A company’s success can also be impacted by its competitors’ actions and even competitors’ reactions to strategy implementation.

Market Demand

A company’s success will depend partly on the market demand for its products or services. Demand should absolutely be a part of the strategy formulation.

A company’s success will highly depend on the quality of its products or services and its ability for its products to meet customer needs.

The senior leadership of a company can play a key role in its success, or failure, as they set the vision & direction of the organization.

How Does Company Leadership Play a Critical Part in a Company’s Strategic Success?

Without involved leadership, a strategic plan will more than likely fail. A company’s leadership plays a critical role in strategic success in several ways:

Setting the Direction

A company’s leadership is responsible for setting the organization’s vision and direction and creating a strategic management plan that aligns with that direction.

A company’s Leadership is responsible for ensuring that the necessary resources, such as funding, personnel, and technology, are available to implement the strategic plan.

Communicating the Plan

A company’s leadership communicates the strategic management plan effectively and consistently to all stakeholders, including employees, customers, and investors.

A company’s leadership needs to model the behaviors and values aligned with the plan and encourage others to do the same.

A company’s leadership needs to provide support & guidance to employees as they work towards achieving the goals and objectives of the strategic plan. This will help in employee retention and strategic success.

A company’s leadership needs to monitor progress toward achieving the goals & objectives of the plan and make necessary adjustments as needed.

A company’s leadership needs to recognize and celebrate successes along the way to help keep team morale high and encourage continued progress to achieve goals.

How Can Companies Prepare & Support their Leaders to Implement & Ensure Strategic Planning Success?

There are many ways in which companies can prepare and support their leaders to implement and ensure the success of their strategic planning initiative.

Provide Proper Training

Companies need to provide training & strategy development opportunities to help their leaders acquire the knowledge and skills they need to implement & support the strategic vision effectively.

Encourage Open Communication

Companies need to foster an environment of open, clear communication and encourage leaders to seek input & feedback from their teams within the strategic framework - even when the strategy map is not positive.

Align Leadership with Company Values

Companies must ensure that their leadership’s values align with the company’s values and culture and that their leaders are committed to the mission and vision of the organization.

Encourage Collaboration

Companies need to encourage collaboration & cross-functional teamwork as a part of project management to ensure that all departments work towards the same goals & objectives.

Provide Resources

As part of the strategic planning process, companies need to ensure their leadership has the necessary resources, such as funding, personnel, & technology, to implement the strategic plan effectively for the entire duration.

Establish Clear Expectations

Companies must set clear expectations for how strategic planning should be activated and implemented and hold leadership accountable for meeting expectations as per the strategic plan document.

Monitor Progress

Company leaders need to monitor the progress toward achieving the goals and objectives of the strategic plan and provide their support and guidance as needed. Strategic planning is essential for business success, and the key to achieving successful results lies in the hands of leadership. For leaders to ensure a strategy’s success, they must become strategic planners and the details of the business’s strategic plan must be organized and understood by each person responsible.

Leaders and managers need to communicate the strategic plan through consistent discussions that foster collaborative decision-making. Responsibilities for the planning process and success also extend beyond the leader and onto each individual employee to help realize the steps of an effective strategic plan. Companies must set clear strategic objectives that align with their mission and strategic goals while preparing business leaders to carry out those plans. When done correctly, with careful attention paid to all levels of the organization, successful strategic planning can lead a company in the right direction toward long-term sustainability and future opportunities.

Having a clear strategic plan is one of those obvious items that every company should have in place yet many companies don’t.

Although the effort of investing the time and resources into creating a strategic planning template can be demanding, the value and impact of your investment can return a healthy multiple.

Once your mission and vision statements and strategic plan are in place they become a touchstone to focus your business, align teams, and what makes your way of navigating your market and competition unique.

We hope that this resource provides a road map and helps facilitate the development of your strategic plan if you don’t have one yet. For those that do have strategic plans, we hope this resource helps act as a checklist to fortify the strategy development you’ve already created.

What is Leadership? A Guide To The Core Elements of Great Leadership & Behaviors That Make an Effective Leader

Business Goal Setting: How to Improve Team Performance & Morale

- Micromanagement vs. Leading: Empowering Your Team for Enhanced Productivity

- Thriving Together: The Intersection of Organizational Culture and Employee Well-being

- What is executive coaching? The definition, benefits, process & why even good leaders need coaching

- Emotional intelligence in leadership: what it is & why it's Important

- Imposter syndrome: definition, types, symptoms, causes & strategies

- Self awareness in leadership: the x factor in team performance

- Effective decision-making: skills, process & strategies to improve as a leader

- 360 feedback assessment: what it is, who its for & how to implement at your organization

- Leadership transition: plan, process, challenges & best practices

- Mastering the CEO transition: How to craft an ironclad CEO succession plan & seamlessly transition a new CEO

Let's explore how we can help you achieve your goals

- Product overview

- All features

- App integrations

CAPABILITIES

- project icon Project management

- Project views

- Custom fields

- Status updates

- goal icon Goals and reporting

- Reporting dashboards

- workflow icon Workflows and automation

- portfolio icon Resource management

- Time tracking

- my-task icon Admin and security

- Admin console

- asana-intelligence icon Asana Intelligence

- list icon Personal

- premium icon Starter

- briefcase icon Advanced

- Goal management

- Organizational planning

- Campaign management

- Creative production

- Content calendars

- Marketing strategic planning

- Resource planning

- Project intake

- Product launches

- Employee onboarding

- View all uses arrow-right icon

- Project plans

- Team goals & objectives

- Team continuity

- Meeting agenda

- View all templates arrow-right icon

- Work management resources Discover best practices, watch webinars, get insights

- What's new Learn about the latest and greatest from Asana

- Customer stories See how the world's best organizations drive work innovation with Asana

- Help Center Get lots of tips, tricks, and advice to get the most from Asana

- Asana Academy Sign up for interactive courses and webinars to learn Asana

- Developers Learn more about building apps on the Asana platform

- Community programs Connect with and learn from Asana customers around the world

- Events Find out about upcoming events near you

- Partners Learn more about our partner programs

- Support Need help? Contact the Asana support team

- Asana for nonprofits Get more information on our nonprofit discount program, and apply.

Featured Reads

- Business strategy |

- What is strategic planning? A 5-step gu ...

What is strategic planning? A 5-step guide

Strategic planning is a process through which business leaders map out their vision for their organization’s growth and how they’re going to get there. In this article, we'll guide you through the strategic planning process, including why it's important, the benefits and best practices, and five steps to get you from beginning to end.

Strategic planning is a process through which business leaders map out their vision for their organization’s growth and how they’re going to get there. The strategic planning process informs your organization’s decisions, growth, and goals.

Strategic planning helps you clearly define your company’s long-term objectives—and maps how your short-term goals and work will help you achieve them. This, in turn, gives you a clear sense of where your organization is going and allows you to ensure your teams are working on projects that make the most impact. Think of it this way—if your goals and objectives are your destination on a map, your strategic plan is your navigation system.

In this article, we walk you through the 5-step strategic planning process and show you how to get started developing your own strategic plan.

How to build an organizational strategy

Get our free ebook and learn how to bridge the gap between mission, strategic goals, and work at your organization.

What is strategic planning?

Strategic planning is a business process that helps you define and share the direction your company will take in the next three to five years. During the strategic planning process, stakeholders review and define the organization’s mission and goals, conduct competitive assessments, and identify company goals and objectives. The product of the planning cycle is a strategic plan, which is shared throughout the company.

What is a strategic plan?

![[inline illustration] Strategic plan elements (infographic)](https://assets.asana.biz/transform/7d1f14e4-b008-4ea6-9579-5af6236ce367/inline-business-strategy-strategic-planning-1-2x?io=transform:fill,width:2560&format=webp "major component of the strategic planning process")

A strategic plan is the end result of the strategic planning process. At its most basic, it’s a tool used to define your organization’s goals and what actions you’ll take to achieve them.

Typically, your strategic plan should include:

Your company’s mission statement

Your organizational goals, including your long-term goals and short-term, yearly objectives

Any plan of action, tactics, or approaches you plan to take to meet those goals

What are the benefits of strategic planning?

Strategic planning can help with goal setting and decision-making by allowing you to map out how your company will move toward your organization’s vision and mission statements in the next three to five years. Let’s circle back to our map metaphor. If you think of your company trajectory as a line on a map, a strategic plan can help you better quantify how you’ll get from point A (where you are now) to point B (where you want to be in a few years).

When you create and share a clear strategic plan with your team, you can:

Build a strong organizational culture by clearly defining and aligning on your organization’s mission, vision, and goals.

Align everyone around a shared purpose and ensure all departments and teams are working toward a common objective.

Proactively set objectives to help you get where you want to go and achieve desired outcomes.

Promote a long-term vision for your company rather than focusing primarily on short-term gains.

Ensure resources are allocated around the most high-impact priorities.

Define long-term goals and set shorter-term goals to support them.

Assess your current situation and identify any opportunities—or threats—allowing your organization to mitigate potential risks.

Create a proactive business culture that enables your organization to respond more swiftly to emerging market changes and opportunities.

What are the 5 steps in strategic planning?

The strategic planning process involves a structured methodology that guides the organization from vision to implementation. The strategic planning process starts with assembling a small, dedicated team of key strategic planners—typically five to 10 members—who will form the strategic planning, or management, committee. This team is responsible for gathering crucial information, guiding the development of the plan, and overseeing strategy execution.

Once you’ve established your management committee, you can get to work on the planning process.

Step 1: Assess your current business strategy and business environment

Before you can define where you’re going, you first need to define where you are. Understanding the external environment, including market trends and competitive landscape, is crucial in the initial assessment phase of strategic planning.

To do this, your management committee should collect a variety of information from additional stakeholders, like employees and customers. In particular, plan to gather:

Relevant industry and market data to inform any market opportunities, as well as any potential upcoming threats in the near future.

Customer insights to understand what your customers want from your company—like product improvements or additional services.

Employee feedback that needs to be addressed—whether about the product, business practices, or the day-to-day company culture.

Consider different types of strategic planning tools and analytical techniques to gather this information, such as:

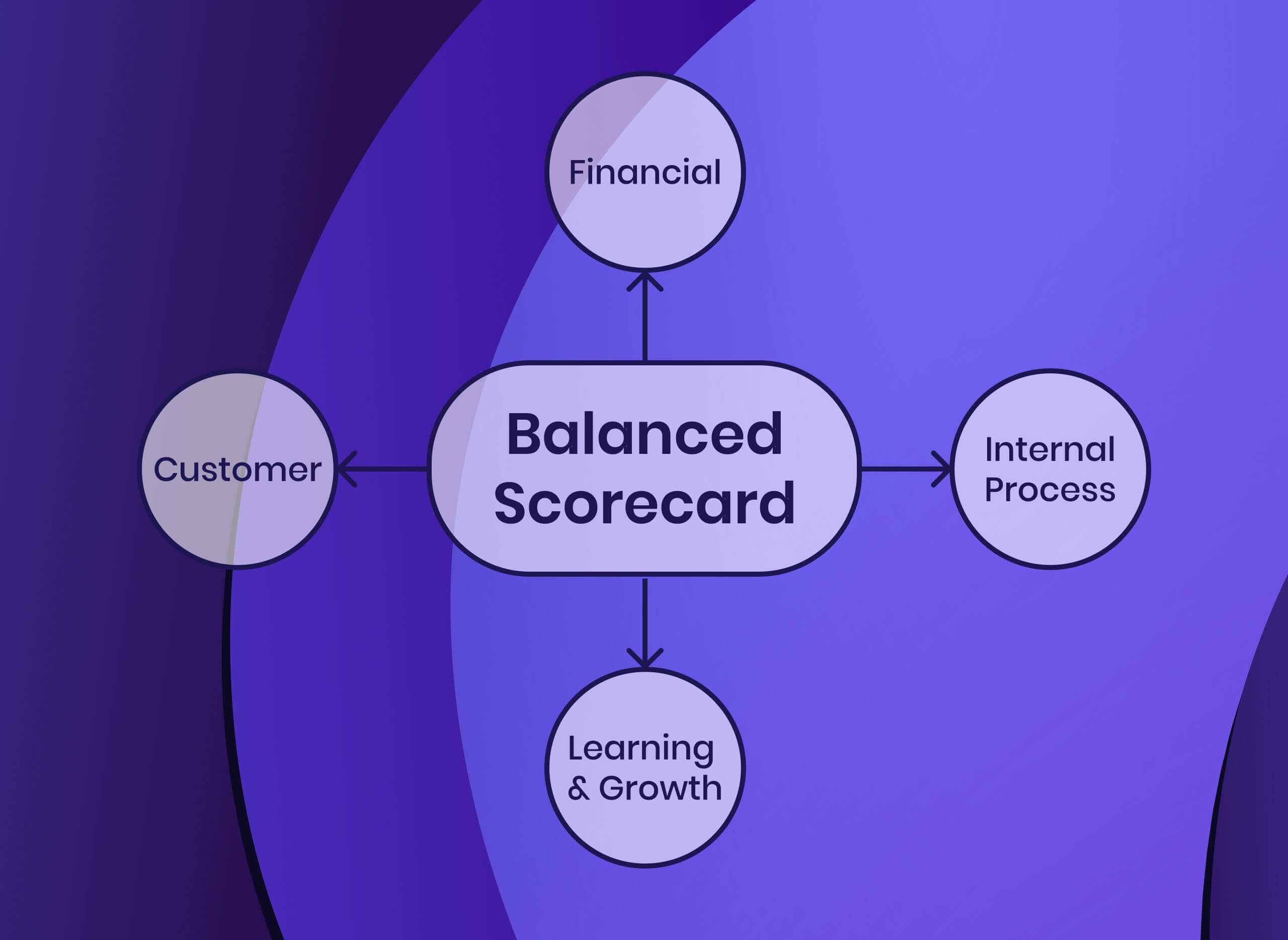

A balanced scorecard to help you evaluate four major elements of a business: learning and growth, business processes, customer satisfaction, and financial performance.

A SWOT analysis to help you assess both current and future potential for the business (you’ll return to this analysis periodically during the strategic planning process).

To fill out each letter in the SWOT acronym, your management committee will answer a series of questions:

What does your organization currently do well?

What separates you from your competitors?

What are your most valuable internal resources?

What tangible assets do you have?

What is your biggest strength?

Weaknesses:

What does your organization do poorly?

What do you currently lack (whether that’s a product, resource, or process)?

What do your competitors do better than you?

What, if any, limitations are holding your organization back?

What processes or products need improvement?

Opportunities:

What opportunities does your organization have?

How can you leverage your unique company strengths?

Are there any trends that you can take advantage of?

How can you capitalize on marketing or press opportunities?

Is there an emerging need for your product or service?

What emerging competitors should you keep an eye on?

Are there any weaknesses that expose your organization to risk?

Have you or could you experience negative press that could reduce market share?

Is there a chance of changing customer attitudes towards your company?

Step 2: Identify your company’s goals and objectives

To begin strategy development, take into account your current position, which is where you are now. Then, draw inspiration from your vision, mission, and current position to identify and define your goals—these are your final destination.

To develop your strategy, you’re essentially pulling out your compass and asking, “Where are we going next?” “What’s the ideal future state of this company?” This can help you figure out which path you need to take to get there.

During this phase of the planning process, take inspiration from important company documents, such as:

Your mission statement, to understand how you can continue moving towards your organization’s core purpose.

Your vision statement, to clarify how your strategic plan fits into your long-term vision.

Your company values, to guide you towards what matters most towards your company.

Your competitive advantages, to understand what unique benefit you offer to the market.

Your long-term goals, to track where you want to be in five or 10 years.

Your financial forecast and projection, to understand where you expect your financials to be in the next three years, what your expected cash flow is, and what new opportunities you will likely be able to invest in.

Step 3: Develop your strategic plan and determine performance metrics

Now that you understand where you are and where you want to go, it’s time to put pen to paper. Take your current business position and strategy into account, as well as your organization’s goals and objectives, and build out a strategic plan for the next three to five years. Keep in mind that even though you’re creating a long-term plan, parts of your plan should be created or revisited as the quarters and years go on.

As you build your strategic plan, you should define:

Company priorities for the next three to five years, based on your SWOT analysis and strategy.

Yearly objectives for the first year. You don’t need to define your objectives for every year of the strategic plan. As the years go on, create new yearly objectives that connect back to your overall strategic goals .

Related key results and KPIs. Some of these should be set by the management committee, and some should be set by specific teams that are closer to the work. Make sure your key results and KPIs are measurable and actionable. These KPIs will help you track progress and ensure you’re moving in the right direction.

Budget for the next year or few years. This should be based on your financial forecast as well as your direction. Do you need to spend aggressively to develop your product? Build your team? Make a dent with marketing? Clarify your most important initiatives and how you’ll budget for those.

A high-level project roadmap . A project roadmap is a tool in project management that helps you visualize the timeline of a complex initiative, but you can also create a very high-level project roadmap for your strategic plan. Outline what you expect to be working on in certain quarters or years to make the plan more actionable and understandable.

Step 4: Implement and share your plan

Now it’s time to put your plan into action. Strategy implementation involves clear communication across your entire organization to make sure everyone knows their responsibilities and how to measure the plan’s success.

Make sure your team (especially senior leadership) has access to the strategic plan, so they can understand how their work contributes to company priorities and the overall strategy map. We recommend sharing your plan in the same tool you use to manage and track work, so you can more easily connect high-level objectives to daily work. If you don’t already, consider using a work management platform .

A few tips to make sure your plan will be executed without a hitch:

Communicate clearly to your entire organization throughout the implementation process, to ensure all team members understand the strategic plan and how to implement it effectively.

Define what “success” looks like by mapping your strategic plan to key performance indicators.

Ensure that the actions outlined in the strategic plan are integrated into the daily operations of the organization, so that every team member's daily activities are aligned with the broader strategic objectives.

Utilize tools and software—like a work management platform—that can aid in implementing and tracking the progress of your plan.

Regularly monitor and share the progress of the strategic plan with the entire organization, to keep everyone informed and reinforce the importance of the plan.

Establish regular check-ins to monitor the progress of your strategic plan and make adjustments as needed.

Step 5: Revise and restructure as needed

Once you’ve created and implemented your new strategic framework, the final step of the planning process is to monitor and manage your plan.

Remember, your strategic plan isn’t set in stone. You’ll need to revisit and update the plan if your company changes directions or makes new investments. As new market opportunities and threats come up, you’ll likely want to tweak your strategic plan. Make sure to review your plan regularly—meaning quarterly and annually—to ensure it’s still aligned with your organization’s vision and goals.

Keep in mind that your plan won’t last forever, even if you do update it frequently. A successful strategic plan evolves with your company’s long-term goals. When you’ve achieved most of your strategic goals, or if your strategy has evolved significantly since you first made your plan, it might be time to create a new one.

Build a smarter strategic plan with a work management platform

To turn your company strategy into a plan—and ultimately, impact—make sure you’re proactively connecting company objectives to daily work. When you can clarify this connection, you’re giving your team members the context they need to get their best work done.

A work management platform plays a pivotal role in this process. It acts as a central hub for your strategic plan, ensuring that every task and project is directly tied to your broader company goals. This alignment is crucial for visibility and coordination, allowing team members to see how their individual efforts contribute to the company’s success.

By leveraging such a platform, you not only streamline workflow and enhance team productivity but also align every action with your strategic objectives—allowing teams to drive greater impact and helping your company move toward goals more effectively.

Strategic planning FAQs

Still have questions about strategic planning? We have answers.

Why do I need a strategic plan?

A strategic plan is one of many tools you can use to plan and hit your goals. It helps map out strategic objectives and growth metrics that will help your company be successful.

When should I create a strategic plan?

You should aim to create a strategic plan every three to five years, depending on your organization’s growth speed.

Since the point of a strategic plan is to map out your long-term goals and how you’ll get there, you should create a strategic plan when you’ve met most or all of them. You should also create a strategic plan any time you’re going to make a large pivot in your organization’s mission or enter new markets.

What is a strategic planning template?

A strategic planning template is a tool organizations can use to map out their strategic plan and track progress. Typically, a strategic planning template houses all the components needed to build out a strategic plan, including your company’s vision and mission statements, information from any competitive analyses or SWOT assessments, and relevant KPIs.

What’s the difference between a strategic plan vs. business plan?

A business plan can help you document your strategy as you’re getting started so every team member is on the same page about your core business priorities and goals. This tool can help you document and share your strategy with key investors or stakeholders as you get your business up and running.

You should create a business plan when you’re:

Just starting your business

Significantly restructuring your business

If your business is already established, you should create a strategic plan instead of a business plan. Even if you’re working at a relatively young company, your strategic plan can build on your business plan to help you move in the right direction. During the strategic planning process, you’ll draw from a lot of the fundamental business elements you built early on to establish your strategy for the next three to five years.

What’s the difference between a strategic plan vs. mission and vision statements?

Your strategic plan, mission statement, and vision statements are all closely connected. In fact, during the strategic planning process, you will take inspiration from your mission and vision statements in order to build out your strategic plan.

Simply put:

A mission statement summarizes your company’s purpose.

A vision statement broadly explains how you’ll reach your company’s purpose.

A strategic plan pulls in inspiration from your mission and vision statements and outlines what actions you’re going to take to move in the right direction.

For example, if your company produces pet safety equipment, here’s how your mission statement, vision statement, and strategic plan might shake out:

Mission statement: “To ensure the safety of the world’s animals.”

Vision statement: “To create pet safety and tracking products that are effortless to use.”

Your strategic plan would outline the steps you’re going to take in the next few years to bring your company closer to your mission and vision. For example, you develop a new pet tracking smart collar or improve the microchipping experience for pet owners.

What’s the difference between a strategic plan vs. company objectives?

Company objectives are broad goals. You should set these on a yearly or quarterly basis (if your organization moves quickly). These objectives give your team a clear sense of what you intend to accomplish for a set period of time.

Your strategic plan is more forward-thinking than your company goals, and it should cover more than one year of work. Think of it this way: your company objectives will move the needle towards your overall strategy—but your strategic plan should be bigger than company objectives because it spans multiple years.

What’s the difference between a strategic plan vs. a business case?

A business case is a document to help you pitch a significant investment or initiative for your company. When you create a business case, you’re outlining why this investment is a good idea, and how this large-scale project will positively impact the business.

You might end up building business cases for things on your strategic plan’s roadmap—but your strategic plan should be bigger than that. This tool should encompass multiple years of your roadmap, across your entire company—not just one initiative.

What’s the difference between a strategic plan vs. a project plan?

A strategic plan is a company-wide, multi-year plan of what you want to accomplish in the next three to five years and how you plan to accomplish that. A project plan, on the other hand, outlines how you’re going to accomplish a specific project. This project could be one of many initiatives that contribute to a specific company objective which, in turn, is one of many objectives that contribute to your strategic plan.

What’s the difference between strategic management vs. strategic planning?

A strategic plan is a tool to define where your organization wants to go and what actions you need to take to achieve those goals. Strategic planning is the process of creating a plan in order to hit your strategic objectives.

Strategic management includes the strategic planning process, but also goes beyond it. In addition to planning how you will achieve your big-picture goals, strategic management also helps you organize your resources and figure out the best action plans for success.

Related resources

What is management by objectives (MBO)?

Write better AI prompts: A 4-sentence framework

How to find alignment on AI

What is content marketing? A complete guide

Strategic Planning Process: Why Is Strategic Planning Important for Organizations in 2024?

What to read next:

Playing chess without a strong opening is a guaranteed way to disadvantage yourself. Just like in chess, organizations without an adequate strategic planning process are unlikely to thrive and adapt long-term.

The strategic planning process is essential for aligning your organization on key priorities, goals, and initiatives, making it crucial for organizational success.

This article will empower you to craft and perfect your strategic planning process by exploring the following:

- What is strategic planning

- Why strategic planning is important for your business

- The seven steps of the strategic planning process

Strategic planning frameworks

- Best practices supporting the strategic planning process

By the end of this article, you’ll have the knowledge needed to perfect the key elements of strategic planning. Ready? Let’s begin.

What is strategic planning?

Strategic planning charts your business's course toward success. Using your organization’s vision, mission statement , and values — with internal and external information — each step of the strategic planning process helps you craft long-term objectives and attain your goals with strategic management.

The key elements of strategic planning includes a SWOT analysis, goal setting , stakeholder involvement, plus developing actionable strategies, approaches, and tactics aligned with primary objectives.

In short, the strategic planning process bridges the gap between your organization’s current and desired state, providing a clear and actionable framework that answers: Where are you now? Where do you want to be? How will you get there?

7 key elements of strategic planning

The following strategic planning components work together to create cohesive strategic plans for your business goals. Let’s take a close look at each of these:

- Vision : What your organization wants to achieve in the future, the long-term goal

- Mission : The driving force behind why your company exists, who it serves, and how it creates value

- Values : Fundamental beliefs guiding your company’s decision-making process

- Goals : Measurable objectives in alignment with your business mission, vision, and values

- Strategy : A long-term strategy map for achieving your objectives based on both internal and external factors

- Approach : How you execute strategy and achieve objectives using actions and initiatives

- Tactics : Granular short-term actions, programs, and activities

Why is the strategic planning process important?

Just as a chess player needs a gameplan to reach checkmate, a company needs a solid strategic plan to achieve its goals.

Without a strategic plan, your business will waste precious time, energy, and resources on endeavors that won’t get your company closer to where it needs to be.

Your ideal plan should cover all key strategic planning areas, while allowing you to stay present by measuring success and course-correcting or redefining the strategic direction when necessary. Ultimately, enabling your company to stay future-proof through the creation of an always-on strategy that reflects your company's mission and vision.

An always-on strategy involves continuous environmental scanning even after the strategic plan has been devised, ensuring readiness to adapt in response to quick, drastic changes in the environment.

Let’s dive deeper into the steps of the strategic planning process.

What are the 7 stages of the strategic planning process?

You understand the overall value of implementing a strategic planning process — now let’s put it in practice. Here's our 7-step approach to strategic planning that ensures everyone is on the same page:

- Clarify your vision, mission, and values

- Conduct an environmental scan

- Define strategic priorities

- Develop goals and metrics

- Derive a strategic plan

- Write and communicate your strategic plan

- Implement, monitor, and revise

1. Clarify your vision, mission, and values

The first step of the strategic planning process is understanding your organization’s core elements: vision, mission, and values. Clarifying these will align your strategic plan with your company’s definition of success. Once established, these are the foundation for the rest of the strategic planning process.

Questions to ask:

- What do we aspire to achieve in the long term?

- What is our purpose or ultimate goal?

- What do we do to fulfill our vision?

- What key activities or services do we provide?

- What are our organization's ethics?

- What qualities or behaviors do we expect from employees?

Read more: What is Mission vs. Vision

2. Conduct an environmental scan

Once everyone on the same page about vision, mission, and values, it's time to scan your internal and external environment. This involves a long-term SWOT analysis, evaluating your organization’s strengths, weaknesses, opportunities, and threats.

Internal factors

Internal strengths and weaknesses help you understand where your organization excels and what it could improve. Strengths and weaknesses awareness helps make more informed decisions with your capabilities and resource allocation in mind.

External factors

Externally, opportunities and threats in the market help you understand the power of your industry’s customers, suppliers, and competitors. Additionally, consider how broader forces like technology, culture, politics, and regulation may impact your organization.

- What are our organization's key strengths or competitive advantages?

- What areas or functions within our organization need improvement?

- What emerging trends or opportunities can we leverage?

- How do changes in technology, regulations, or consumer behavior impact us?

3. Define strategic priorities

Prioritization puts the “strategic” in strategic planning process. Your organization’s mission, vision, values, and environmental scan serve as a lens to identify top priorities. Limiting priorities ensures your organization intentionally allocates resources.

These categories can help you rank your strategic priorities:

- Critical : Urgent tasks whose failure to complete will have severe consequences — financial losses, reputation damage, or legal consequences

- Important : Significant tasks which support organizational achievements and require timely completion

- Desirable : Valuable tasks not essential in the short-term, but can contribute to long-term success and growth

- How do these priorities align with our mission, vision, and values?

- Which tasks need to be completed quickly to ensure effective progress towards our desired outcomes?

- What resources and capabilities do we need to pursue these priorities effectively?

4. Develop goals and metrics

Next, you establish goals and metrics to reflect your strategic priorities. Purpose-driven, long-term, actionable strategic planning goals should flow down through the organization, with lower-level goals contributing to higher-level ones.

One approach that can help you set and measure your aligned goals is objectives and key results (OKRs). OKRs consist of objectives, qualitative statements of what you want to achieve, and key results, 3-5 supporting metrics that track progress toward your objective.

OKRs ensure alignment at every level of the organization, with tracking and accountability built into the framework to keep everyone engaged. With ambitious, intentional goals, OKRs can help you drive the strategic plan forward.

- What metrics can we use to track progress toward each objective?

- How can we ensure that lower-level goals and metrics support and contribute to higher-level ones?

- How will we track and measure progress towards key results?

- How will we ensure accountability?

Get an in-depth look at OKRs with our Ultimate OKR Playbook

5. Derive a strategic plan

The next step of the strategic planning process gets down to the nitty-gritty “how” — developing a clear, practical strategic plan for bridging the gap between now and the future.

To do this, you’ll need to brainstorm short- and long-term approaches to achieving the goals you’ve set, answering a couple of key questions along the way. You must evaluate ideas based on factors like:

- Feasibility : How realistic and achievable is it?

- Impact : How conducive is it to goal attainment?

- Cost : Can we fund this approach, and is it worth the investment?

- Alignment : Does it support our mission, vision, and values?

From your approaches, you can devise a detailed action plan, which covers things like:

- Timelines : When will we take each step, and what are the deadlines?

- Milestones : What key achievements will ensure consistent progress?

- Resource requirements : What’s needed to achieve each step?

- Responsibilities : Who's accountable in each step?

- Risks and challenges : What can affect our ability to execute our plan? How will we address these?

With a detailed action plan like this, you can move from abstract goals to concrete steps, bringing you closer to achieving your strategic objectives.

6. Write and communicate your strategic plan